Boeing’s (NYSE:BA) Q1 CY2026 Sales Top Estimates

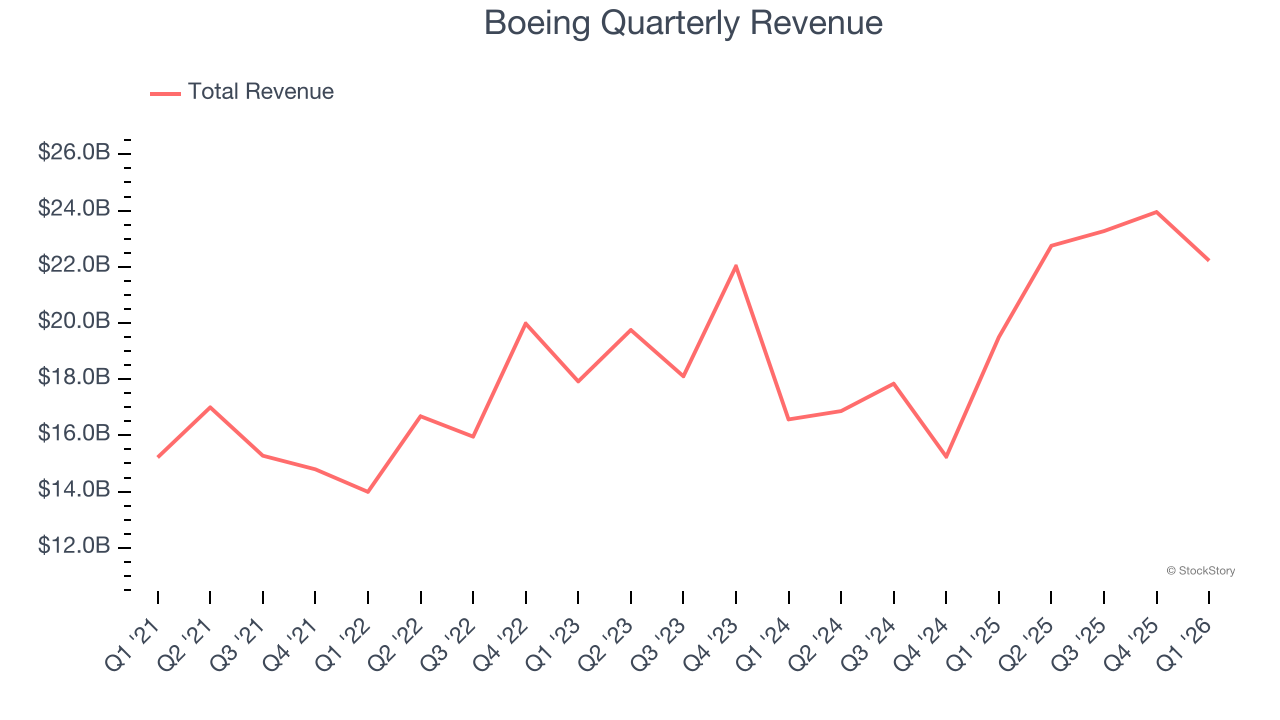

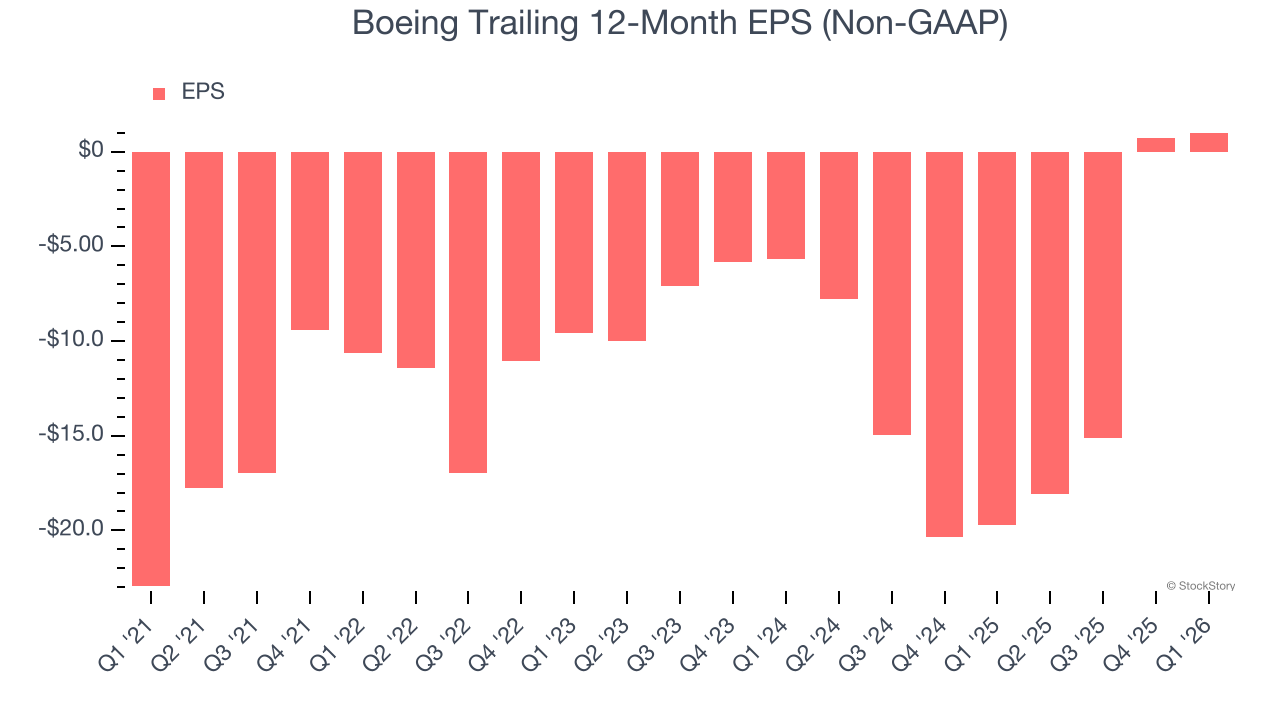

Aerospace and defense company Boeing (NYSE:BA) reported Q1 CY2026 results beating Wall Street’s revenue expectations, with sales up 14% year on year to $22.22 billion. Its non-GAAP loss of $0.20 per share was 70.3% above analysts’ consensus estimates.

Is now the time to buy Boeing? Find out by accessing our full research report, it’s free.

Boeing (BA) Q1 CY2026 Highlights:

- Revenue: $22.22 billion vs analyst estimates of $21.6 billion (14% year-on-year growth, 2.9% beat)

- Adjusted EPS: -$0.20 vs analyst estimates of -$0.67 (70.3% beat)

- Adjusted Operating Income: $448 million vs analyst estimates of $291.8 million (2% margin, 53.5% beat)

- Expects certification of the long-delayed 737 Max 7 and Max 10 later this year, with deliveries starting in 2027

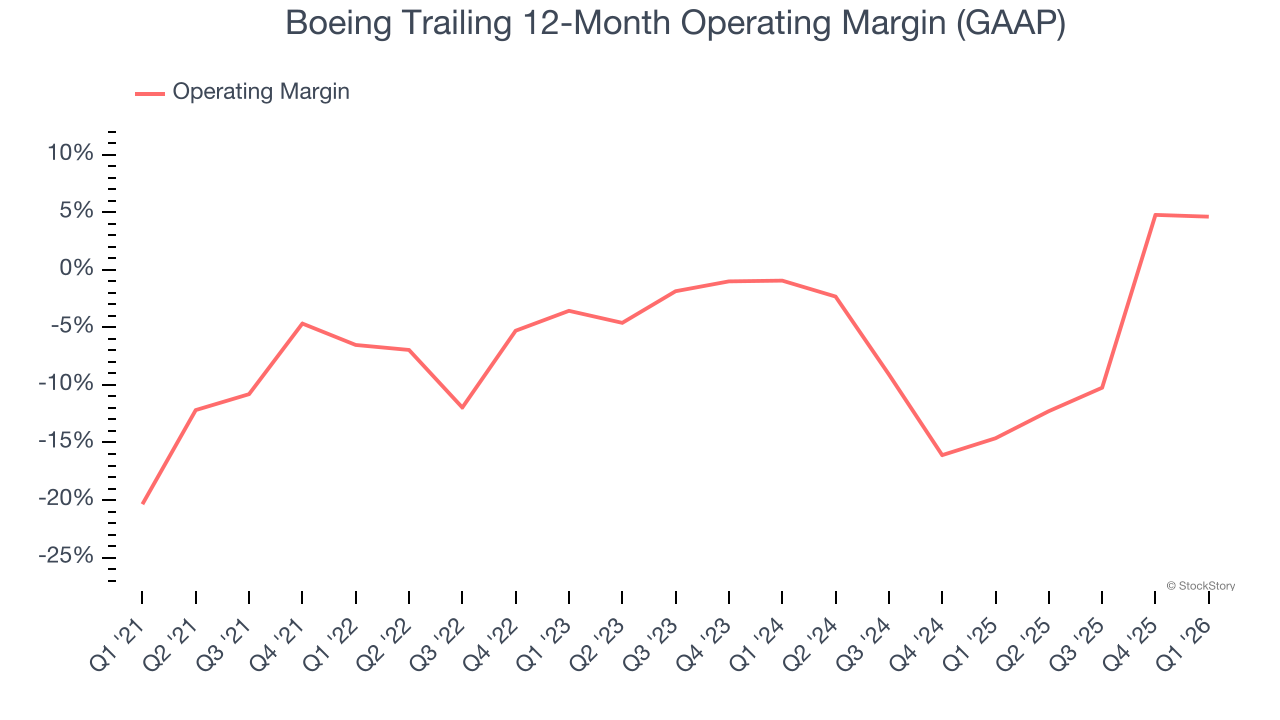

- Operating Margin: 2%, in line with the same quarter last year

- Backlog: $694.7 billion at quarter end, up 27.5% year on year

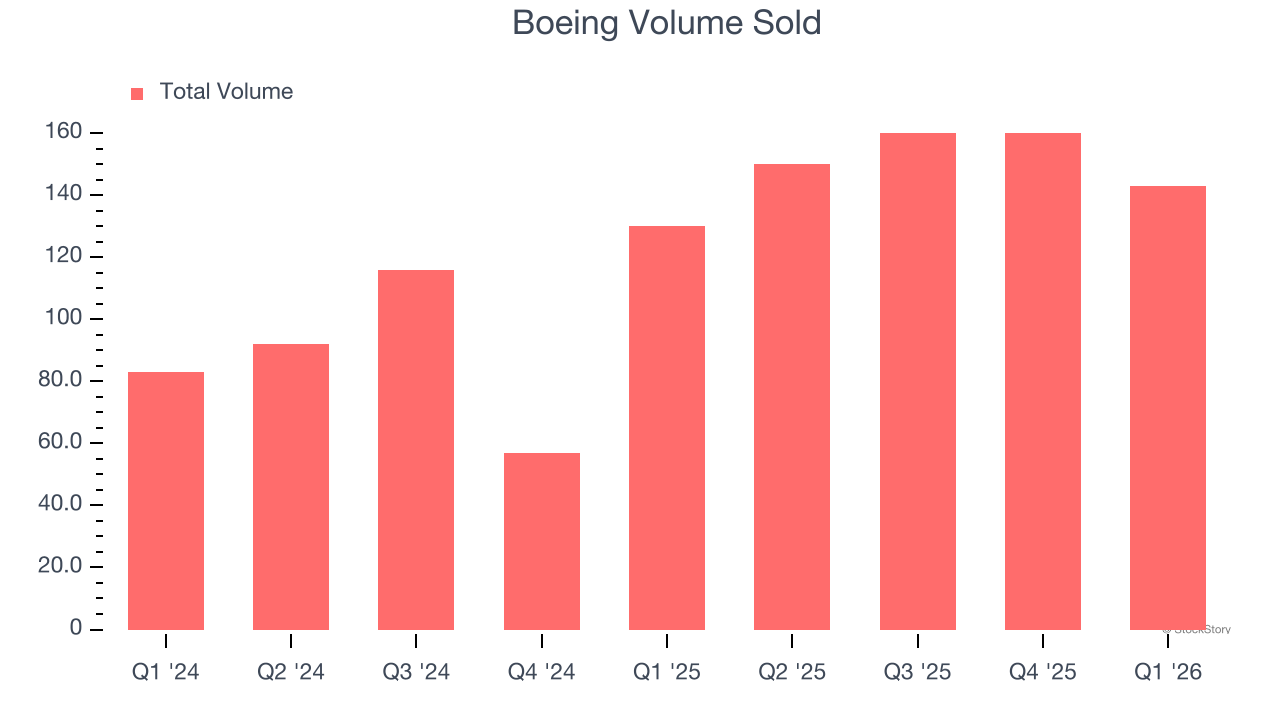

- Sales Volumes rose 10% year on year (56.6% in the same quarter last year)

- Market Capitalization: $172.2 billion

"We're building on our momentum with a strong start to the year and growing record-breaking backlog across our business, while supporting our customers with inspiring missions like Artemis II," said Kelly Ortberg, Boeing president and chief executive officer.

Company Overview

One of the companies that forms a duopoly in the commercial aircraft market, Boeing (NYSE:BA) develops, manufactures, and services commercial airplanes, defense products, and space systems.

Revenue Growth

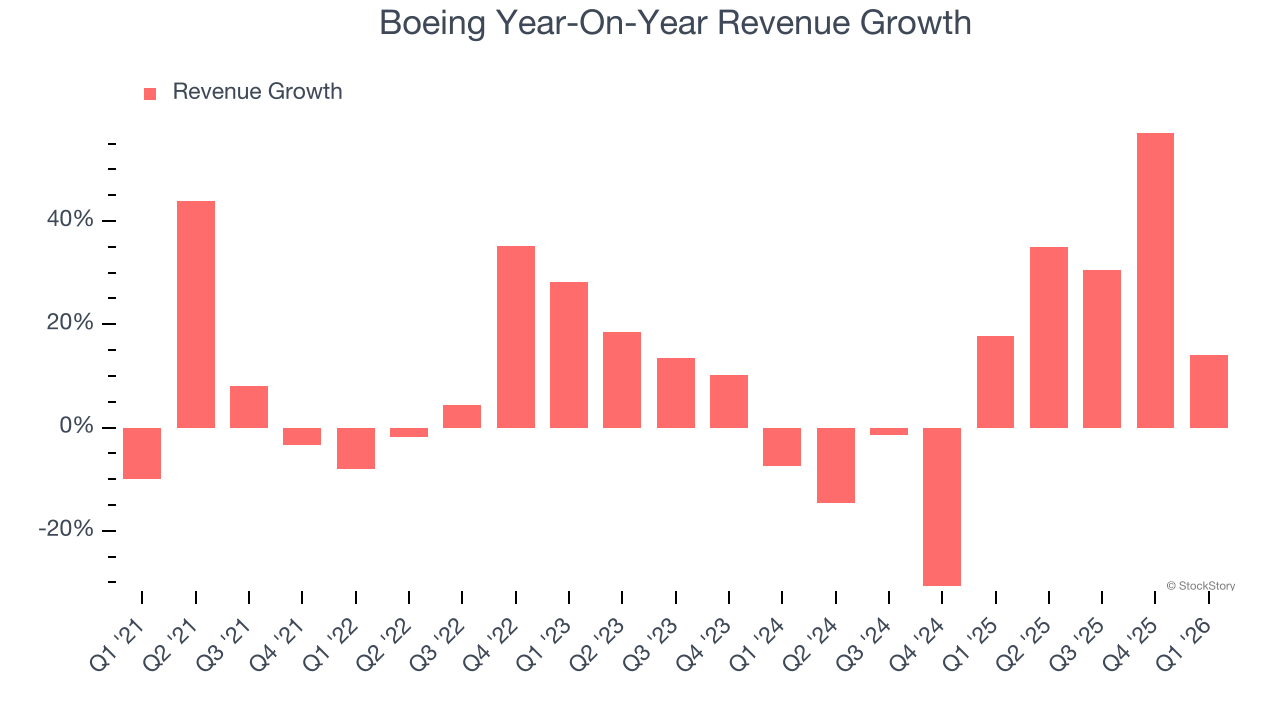

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, Boeing’s sales grew at a solid 10.3% compounded annual growth rate over the last five years. Its growth beat the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Boeing’s annualized revenue growth of 9.8% over the last two years aligns with its five-year trend, suggesting its demand was predictably strong.

Boeing also reports its number of units sold, which reached 143 in the latest quarter. Over the last two years, Boeing’s units sold averaged 69.7% year-on-year growth. Because this number is better than its revenue growth, we can see the company’s average selling price decreased.

This quarter, Boeing reported year-on-year revenue growth of 14%, and its $22.22 billion of revenue exceeded Wall Street’s estimates by 2.9%.

Looking ahead, sell-side analysts expect revenue to grow 9% over the next 12 months, similar to its two-year rate. This projection is above average for the sector and implies its newer products and services will help maintain its recent top-line performance.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Operating Margin

Although Boeing was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 3.5% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, Boeing’s operating margin rose by 11.1 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to show consistent profitability.

In Q1, Boeing generated an operating margin profit margin of 2%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Boeing’s full-year EPS flipped from negative to positive over the last five years. This is a good sign and shows it’s at an inflection point.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Boeing, its two-year annual EPS growth of 47.6% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q1, Boeing reported adjusted EPS of negative $0.20, up from negative $0.49 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Boeing’s full-year EPS of $1.01 to shrink by 2.9%.

Key Takeaways from Boeing’s Q1 Results

It was good to see Boeing beat analysts’ operating income and EPS expectations this quarter. We were also excited that the company expects certification of the long-delayed 737 Max 7 and Max 10 later this year, with deliveries starting in 2027. Zooming out, we think this was a solid print. The stock traded up 3.2% to $226.62 immediately after reporting.

Indeed, Boeing had a rock-solid quarterly earnings result, but is this stock a good investment here? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).