Why Costco's E-commerce Gains Could Drive Higher Valuation

Costco Wholesale Corporation’s COST rapidly expanding e-commerce business is increasingly becoming a factor that could support a richer market valuation for the retailer. While the company has long been associated with warehouse traffic and membership loyalty, the latest sales update suggests its digital business is now contributing to growth in a more material way.

Digitally enabled comparable sales increased 18.8% in April and climbed 21.6% for the first 35 weeks ended May 3, 2026. Even after adjusting for gasoline prices and foreign exchange, digitally enabled comparable sales still rose 18.4% in April and 21.1% for the first 35 weeks. Those figures significantly outpaced the company’s overall comparable sales growth of 11.6%, indicating that Costco’s online ecosystem is scaling faster than its core warehouse business.

Strong digital momentum suggests that Costco is expanding customer engagement beyond in-store bulk shopping while reinforcing convenience for existing members. The company’s e-commerce presence now spans several international markets, including the United States, Canada, the United Kingdom, Mexico, Korea, Taiwan, Japan and Australia.

In an environment marked by inflationary pressures and uncertain consumer spending patterns, Costco’s digital growth may be strengthening investor confidence that the retailer can sustain revenue growth across multiple shopping channels. The acceleration of these digital channels serves as a powerful catalyst for a higher valuation because it diversifies revenue streams and captures a broader share of member spending.

What the Latest Metrics Say About Costco's Valuation

From a valuation standpoint, Costco's forward 12-month price-to-earnings ratio stands at 46.37, higher than the industry’s ratio of 32.36 but below its median P/E level of 46.88, observed over the past year. Although the premium multiple may appear elevated, investors often view Costco as a high-quality retail operator supported by resilient comparable sales growth, strong membership retention and expanding digital capabilities.

As long as Costco continues to deliver consistent sales growth and strengthen its omnichannel presence, its premium valuation could remain supported by investors seeking stable growth within the retail sector.

Image Source: Zacks Investment Research

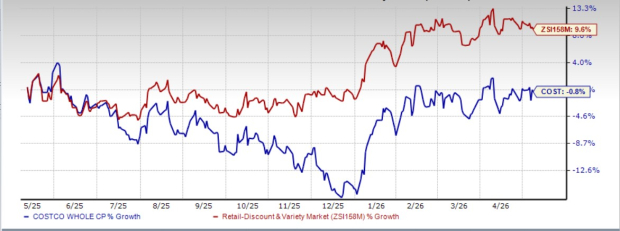

Shares of Costco have fallen 0.8% over the past year against the Retail – Discount Stores industry’s 9.6% rise.

Image Source: Zacks Investment Research

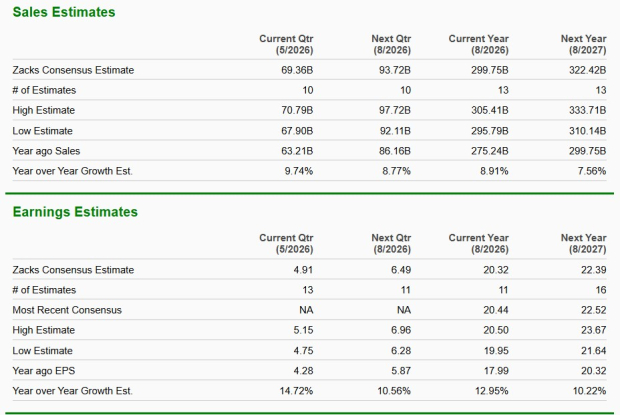

The Zacks Consensus Estimate for Costco’s current financial-year sales and earnings per share implies year-over-year growth of 8.9% and 13%, respectively. For the next fiscal year, the consensus estimate indicates a 7.6% rise in sales and 10.2% growth in earnings.

Image Source: Zacks Investment Research

Costco’s Peer Performance: Walmart & BJ’s Wholesale

Walmart Inc.WMT continues to scale its digital ecosystem aggressively, with e-commerce sales rising 24% globally and contributing 23% of total sales during the fourth quarter of fiscal 2026. Walmart is leveraging store-fulfilled delivery, AI-driven tools and marketplace expansion to enhance convenience and drive higher basket sizes. Walmart’s comparable sales growth of 4.6% in the U.S. division reflects increased customer transactions supported by digital adoption.

BJ's Wholesale Club Holdings, Inc.BJ is also seeing robust digital traction, with digitally enabled comparable sales growing 31% during the fourth quarter of fiscal 2025. BJ’s Wholesale benefits from a club-based fulfillment model, with more than 90% of digital orders fulfilled in-club, supporting efficiency. BJ’s Wholesale continues to pair digital growth with membership expansion and traffic gains, reinforcing its omnichannel value proposition.

While Costco and BJ's Wholesale Club each carry a Zacks Rank #3 (Hold), Walmart holds a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).