Can Dollar General Keep Expanding Earnings in Fiscal 2026?

Dollar General Corporation’s DG ability to expand earnings in fiscal 2026 appears increasingly tied to margin improvement rather than aggressive sales acceleration. The company’s first-quarter results offered evidence that this strategy is gaining traction.

Earnings rose 12.4% year over year to $2.00 per share, significantly outpacing the 3.4% increase in sales. The key driver was operating margin expansion, with operating profit climbing 10.8% to $638.5 million. Gross margin improved 65 basis points, supported by higher inventory markups as well as lower shrink and inventory damages. The operating margin expanded 40 basis points despite higher fuel costs and weather-related disruptions.

Management highlighted that shrink reduction remains a meaningful contributor. During the quarter, shrink improved another 28 basis points even against a strong prior-year comparison. Inventory damage trends also came in better than expected. Beyond these gains, the company continues to benefit from category management initiatives, supply-chain productivity improvements and the growing contribution of its DG Media Network.

Dollar General expects these margin drivers to remain active through the remainder of fiscal 2026. While management acknowledged headwinds from elevated fuel costs and tougher year-over-year comparisons, it still anticipates full-year gross margin expansion. We expect gross margin to expand 40 basis points in fiscal 2026. The confidence was strong enough for the company to raise its fiscal 2026 earnings view to $7.20-$7.45 from the prior range of $7.10-$7.35.

The first quarter suggests that earnings growth in fiscal 2026 may depend less on outsized revenue gains and more on Dollar General’s continued success in extracting efficiencies and expanding profitability across its operations.

How Dollar General Compares With Walmart and Target

Walmart Inc.WMT and Target CorporationTGT are also focused on sustaining earnings growth through a combination of sales momentum and margin expansion.

Walmart reported a 5.1% increase in adjusted operating income and an 8.2% rise in adjusted earnings per share in the first quarter of fiscal 2027, supported by strong e-commerce growth, higher-margin advertising revenues and expanding membership income streams. Walmart maintained its fiscal 2027 adjusted operating income growth outlook of 6%-8% and reaffirmed adjusted EPS guidance of $2.75-$2.85, signaling confidence in continued earnings expansion despite elevated fuel costs.

Target is also showing encouraging signs. Target generated a 29.1% increase in adjusted operating income in the first quarter of fiscal 2026, while adjusted earnings per share jumped 32% year over year. Target now expects its full-year operating margin rate to improve by more than 20 basis points versus fiscal 2025 and projects fiscal 2026 earnings near the high end of its prior guidance range of $7.50-$8.50 per share. As Target invests in merchandising, digital capabilities and store enhancements, it appears well-positioned to support further earnings growth.

What the Latest Metrics Say About Dollar General

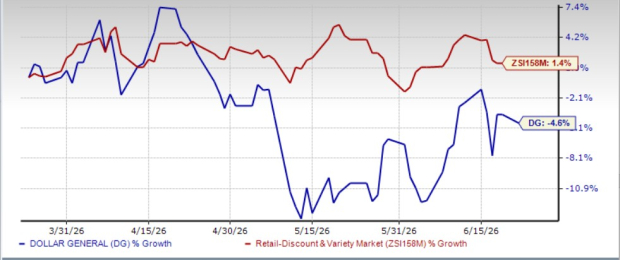

Dollar General has seen its shares tumble 4.6% over the past three months against the industry’s rise of 1.4%.

Image Source: Zacks Investment Research

From a valuation standpoint, Dollar General's forward 12-month price-to-earnings ratio stands at 14.78, lower than the industry’s ratio of 31.25. However, it is trading below its 12-month median level of 17.06.

Image Source: Zacks Investment Research

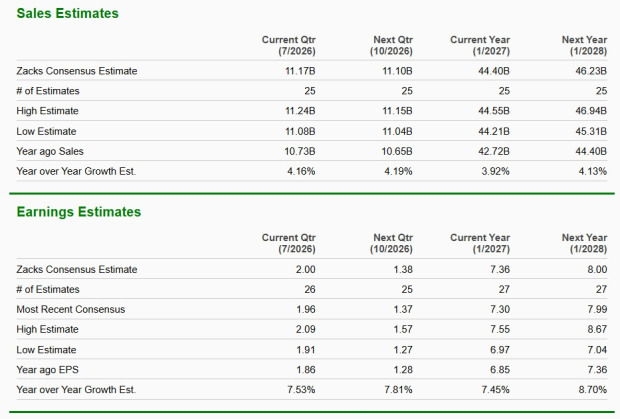

The Zacks Consensus Estimate for Dollar General’s current financial-year sales and earnings per share implies year-over-year growth of 3.9% and 7.5%, respectively. For the next fiscal year, the consensus estimate indicates a 4.1% rise in sales and 8.7% growth in earnings.

Image Source: Zacks Investment Research

Dollar General currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).