Should You Buy, Sell or Hold Honeywell Stock Post Aerospace Spin-Off?

Honeywell TechnologiesHON is in the headlines nowadays as it recently completed a strategic restructuring of its business to operate as a premier pure-play automation company.

On June 29, the company emerged as a separate public company, following the spin-off of the Aerospace Technologies business from Honeywell International. This marked the completion of the company’s multi-year portfolio restructuring actions, separating into three stand-alone publicly traded companies. This enables Honeywell to rebalance its portfolio toward the industrial automation business and flourish through better operational focus, capital allocation policies and financial flexibility.

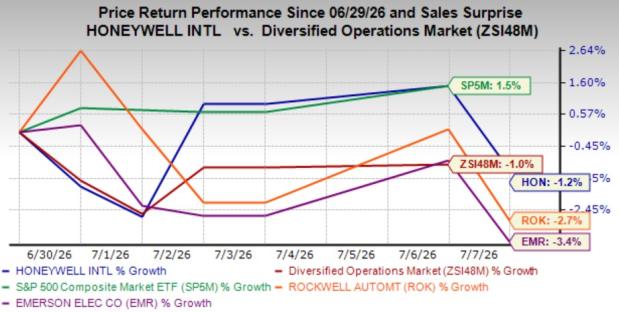

HON’s Price Performance

Image Source: Zacks Investment Research

Following the spin-off of the Aerospace Technologies business, HON’s shares have inched down 1.2% compared with the Zacks Diversified Operations industry’s 1% decline and the S&P 500’s 1.5% growth. Shares of its key rivals like Rockwell AutomationROK and Emerson Electric Co.EMR are down 2.7% and 3.4%, respectively, over the same time frame.

Closing at $225.05 in the last trading session, the stock is trading below its 52-week high of $260.28 but higher than its 52-week low of $195.87. The recent business portfolio transformation move led some investors to wonder whether to buy, sell or hold the stock. Let’s understand the company’s competency as a leading automation player to better analyze how to play the stock.

Factors Influencing Honeywell’s Performance

Investors can take confidence from the fact that Honeywell is witnessing strong momentum across its businesses. In the first quarter of 2026, organic revenues from the company’s Building Automation segment increased 8% year over year. The results were driven by solid demand for its products and solutions, led by increasing building projects, particularly in North America. Increasing order rates and capex investments in data centers and health care projects bode well for it.

Recovery in the Industrial Automation segment, driven by favorable project timing within the warehouse and workflow solutions business, bodes well for the company. The segment’s organic revenues increased 1% year over year in the first quarter. Driven by its business strength, HON expects overall revenues to be in the $19.9-$20.2 billion range in 2026, with organic revenues expected to increase 2-3% on a year-over-year basis.

Honeywell has announced several strategic actions over the past year to boost its organic growth and simplify its business portfolio. In February 2026, Honeywell inked an amended agreement to acquire Johnson Matthey's Catalyst Technologies Business. The deal was first announced in May 2025. The inclusion of Johnson Matthey's Catalyst Technologies unit will enable Honeywell to strengthen its UOP business and grow its installed base across the petrochemical and refining catalysts.

Also, the company’s acquisition of Nexceris’ Li-ion Tamer business (in July 2025) enabled it to boost its fire life safety portfolio under the Building Automation business and expand its presence across the energy storage and data centers markets.

Honeywell’s commercial and operational excellence initiatives, along with its pricing actions, will likely help it maintain a healthy margin performance. For 2026, it expects segment margin to be in the range of 19.8-20.3%, suggesting a year-over-year expansion of 220-270 basis points. Also, strong free cash flow generation supports the company’s shareholder-friendly activities. It expects free cash flow to be approximately $2 billion for the year.

Few Near-Term Concerns Prevail

Honeywell has been witnessing weakness in the Process Automation and Technology segment. Softness in the UOP business due to lower petrochemical catalyst shipments, as customers continued to defer projects, is concerning for the company. Also, reducing customer demand in the Middle East due to the ongoing conflict resulted in a temporary impact on revenues. In the first quarter of 2026, the segment’s organic revenues decreased 6% on a year-over-year basis.

The company has also been subject to high costs and expenses related to increased direct and indirect material costs, rising labor costs, investment in digital infrastructure and business integration activities. Escalating expenses, if not controlled, are likely to hurt the company’s bottom line in the quarters ahead.

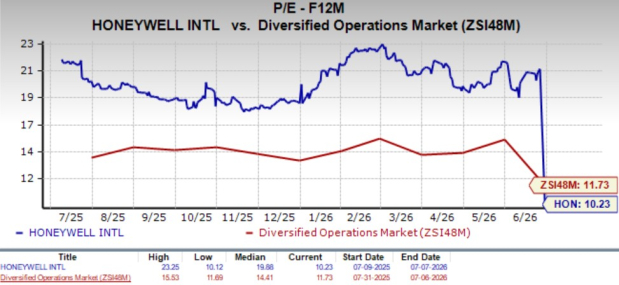

Stock Valuation

Image Source: Zacks Investment Research

Honeywell is currently trading at a forward 12-month P/E of 10.23X, a discount compared with the industry’s 11.73X. The stock is also cheap when compared with its peers, Rockwell Automation and Emerson Electric. Notably, Rockwell Automation and Emerson Electric are currently trading at 32.98X and 19.72X, respectively.

Should You Invest in HON Right Now?

Despite Honeywell’s several upsides and impressive dividend payout trend, the near-term challenges, such as weakness in the Process Automation and Technology unit and rising costs and expenses, are limiting this Zacks Rank #3 (Hold) company’s near-term prospects. While current shareholders should hold their positions, new investors should wait for the stock to retract some of its recent gains and provide a better entry point. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).