ExxonMobil vs. Enterprise Products: Which Energy Giant Has the Edge?

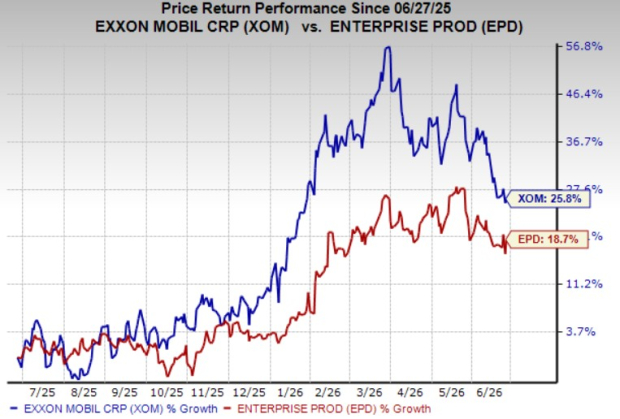

Exxon Mobil CorporationXOM and Enterprise Products Partners LPEPD are two giants in the energy space. Over the past year, XOM has rallied 25.8%, outperforming EPD’s 18.7% gain. Does it mean that ExxonMobil is a better stock? Let’s delve deeper.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Price is not the only parameter to underline the attractiveness of any stock, although it reflects investors’ preferences in every business phase. Hence, before coming to investment conclusions, we need to analyze the fundamentals and overall business environment of both companies.

Softer Oil to Hurt ExxonMobil’s Upstream Business

West Texas Intermediate (“WTI”) oil is currently hovering around $70 per barrel, according to data from Oilprice.com, significantly lower than the more than $100 per barrel reached in May this year, as the oil flows through the Strait of Hormuz are recovering, with shipping activity picking up again since the United States and Iran reached an interim deal last week. This is relatively hurting the upstream business of integrated energy players like ExxonMobil.

The advantageous assets in which XOM operates include the Permian, the most prolific basin in the United States, and offshore Guyana resources. Although the assets have cost advantages, softer oil prices are likely to lower the integrated energy giant’s bottom line, as upstream operations contribute the most to its earnings.

Enterprise Products’ Resilience Business Model

Unlike most energy players, Enterprise Products Partners’ business is not highly vulnerable to fluctuations in commodity prices.

This is because Enterprise Products Partners is a leading midstream player, and therefore, it has a resilient business model. EPD has a pipeline network that spans more than 50,000 miles, transporting oil, natural gas, refined products and other commodities. Thus, the partnership generates stable fee-based revenues from the midstream assets, irrespective of the volatility in commodity prices, as the assets are booked by shippers for a long term.

Due to the resilience of its business model, the partnership has been able to return capital to unitholders on an ongoing basis. Since its IPO, Enterprise Products has returned billions to unitholders through both repurchases and distributions.

EPD vs. XOM: Which Stock to Bet On?

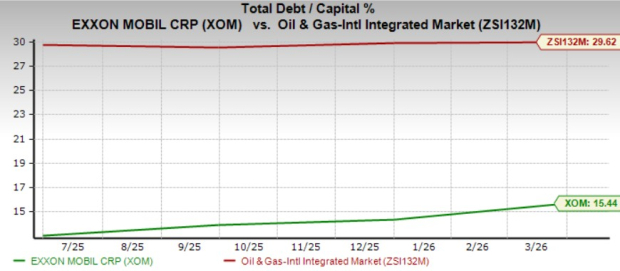

The softer oil pricing environment will likely hurt the exploration and production activities of XOM, although the energy major can lean on its strong balance sheet to sail through the relatively unfavorable business environment. XOM’s debt-to-capitalization of 15.4% is significantly lower than the industry’s 29.6%.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

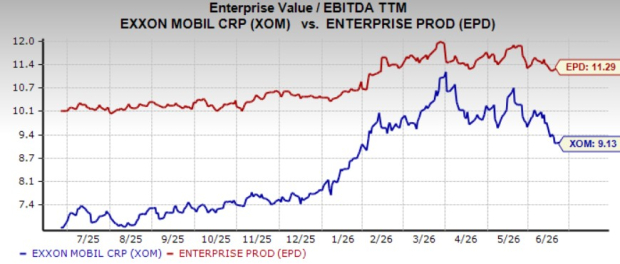

Considering the valuation snapshot, it has become evident that investors are now willing to pay a premium for EPD over XOM, as they are probably preferring a stable midstream business model over upstream operations, especially in the softer oil pricing scenario. The overvaluation is reflected in the fact that Enterprise Products trades at a trailing 12-month enterprise value to EBITDA (EV/EBITDA) of 11.29X, above XOM’s 9.13X.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Thus, investors willing to avoid commodity price volatility and already invested in EPD can hold the stock, currently carrying a Zacks Rank #3 (Hold). Investors who like taking risks can continue to stay invested in XOM, which also has a Zacks Rank of 3. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).