Micron Q3 Earnings Beat Estimates, Revenues Rise on AI Memory Strength

Micron TechnologyMU reported third-quarter fiscal 2026 non-GAAP earnings of $25.11 per share, beating the Zacks Consensus Estimate by 17.39%. The company reported earnings of $1.91 per share in the year-ago quarter.

Revenues soared 345.7% year over year to $41.46 billion and surpassed the Zacks Consensus Estimate by 12.91%. Revenues jumped 73.7% sequentially. The upside was driven by robust AI-led memory demand, with data center revenues exceeding $25 billion, an annualized run rate of more than $100 billion.

Micron announced 16 strategic customer agreements (SCAs) across data center, consumer and auto markets in the reported quarter. These agreements represent roughly 20% of DRAM volume and one-third of NAND volume over the covered period.

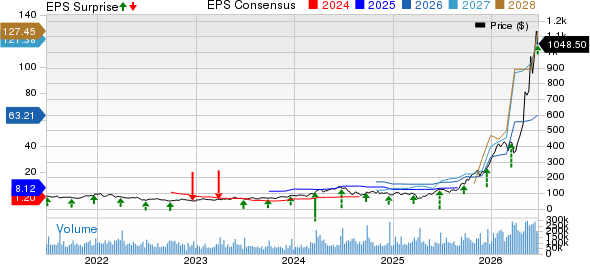

Micron Technology, Inc. Price, Consensus and EPS Surprise

Micron Technology, Inc. price-consensus-eps-surprise-chart | Micron Technology, Inc. Quote

The company expects approximately half or more of its revenues to eventually be under SCAs. Under the agreements signed so far, Micron projects $22 billion in cash deposits and related financial commitments, supporting longer-term supply visibility and financial predictability.

MU’s Q3 Top-Line Details

Micron’s top-line growth benefited from tight DRAM and NAND supply, stronger pricing and accelerating demand tied to AI infrastructure. MU noted that industry demand for both DRAM and NAND continues to significantly exceed supply.

DRAM revenues were $31.3 billion, accounting for 76% of total revenues in the fiscal third quarter. DRAM revenues increased 67% sequentially, helped by low-single-digit bit shipment growth and a low-60s percentage increase in average selling price (ASP).

NAND revenues were $9.9 billion, representing 24% of total revenues. NAND revenues increased 99% sequentially, driven by a mid-single-digit increase in bit shipments and a mid-80s percentage rise in ASP.

MU’s Business Units Set Records

Cloud Memory Business Unit revenues were a record $13.77 billion, up 77.7% sequentially and 306.6% year over year.

Core Data Center Business Unit revenues were a record $11.52 billion, up 103% sequentially and 653.2% year over year.

Mobile and Client Business Unit revenues were a record $11.52 billion, up 49.4% sequentially and 254% year over year. The sequential revenue growth was driven by higher pricing.

Automotive and Embedded Business Unit revenues were a record $4.63 billion, up 71.1% sequentially and 311.2% year over year. The improvement reflected higher pricing and higher bit shipments.

MU’s Q3 Margins Expand

Non-GAAP gross margin was 84.9% in the reported quarter, up from 74.9% in the fiscal second quarter and 39% in the year-ago quarter.

Cloud Memory Business Unit gross margin expanded to 83% from 74% reported in the prior quarter, driven by higher pricing. The company reported Cloud Memory gross margin of 58% in the year-ago quarter. On a sequential basis, the core Data Center Business Unit’s gross margin improved to 87% from 74%, aided by higher pricing and a favorable mix. The company reported Data Center gross margin of 38% in the year-ago quarter.

Mobile and Client Business Unit gross margin reached 87% compared with 79% in the prior quarter and 24% in the year-ago quarter. Automotive and Embedded Business Unit gross margin surged to 79% compared with 68% in the prior quarter and 26% in the year-ago quarter.

Non-GAAP operating expenses were $1.52 billion, up 6.8% year over year and 34% sequentially.

In the third quarter of fiscal 2026, non-GAAP operating income came in at $33.68 billion, a significant rise from $2.49 billion reported in the year-ago quarter and $16.46 billion reported in the previous quarter.

Micron’s Balance Sheet Shows Strong Liquidity Level

MU exited the quarter with $30.2 billion in cash, marketable investments and restricted cash. Liquidity was $32.2 billion at the end of the fiscal third quarter.

Micron generated $25.39 billion in operating cash flow in the quarter. Capital expenditures, net of proceeds from government incentives and asset sales, were $7.1 billion, resulting in adjusted free cash flow of $18.3 billion.

The company declared a quarterly dividend of 15 cents per share, payable on July 21, 2026, to shareholders of record as of July 6. Micron did not repurchase shares during the fiscal third quarter.

MU’s Guidance Points to More Strength

For the fourth quarter of fiscal 2026, Micron expects revenues of $50 billion, plus or minus $1 billion. The company projects a non-GAAP gross margin of approximately 86%.

Non-GAAP operating expenses are expected to be approximately $1.65 billion. Adjusted earnings are projected at $31 per share, plus or minus $1, based on roughly 1.15 billion diluted shares.

Micron now expects supply-demand conditions for both DRAM and NAND to remain tight beyond calendar 2027. In DRAM, the company expects industry DRAM bit shipments in calendar 2026 to grow in the low to mid-20s percentage range, slightly above MU’s prior outlook. In NAND, Micron expects industry NAND bit shipments in calendar 2026 to grow approximately 20%, unchanged from its prior expectations.

Stocks to Consider

Currently, Micron sports a Zacks Rank #1 (Strong Buy).

Some other top-ranked stocks in the broader Zacks Computer and Technology sector are Credo TechnologyCRDO, Hewlett Packard EnterpriseHPE and Microchip TechnologyMCHP. Each of the three stocks sports a Zacks Rank #1 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Long-term earnings growth rate for Credo, Hewlett Packard Enterprise and Microchip is currently pegged at 39.3%, 31.98% and 36.82%, respectively. Year to date, shares of Credo, Hewlett Packard Enterprise and Microchip have jumped 86.9%, 102.9% and 45.1%, respectively.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).