MOS Q1 Earnings Lag Estimates on Higher Input Costs, Sales Up Y/Y

The Mosaic Company MOS posted first-quarter 2026 adjusted earnings of 5 cents per share, down 89.8% from 49 cents a year ago. The figure missed the Zacks Consensus Estimate of 20 cents by 75%.

Net sales rose 14.4% year over year to $2,998 million and beat the consensus estimate of $2,749.3 million by 9%. Results reflected volatile fertilizer and raw material markets.

The Mosaic Company Price, Consensus and EPS Surprise

The Mosaic Company price-consensus-eps-surprise-chart | The Mosaic Company Quote

MOS' Segment Highlights

MOS’ Phosphate segment generated net sales of $1.4 billion in the quarter, up from $1.1 billion a year ago. Sales volumes increased to 1.9 million tons from 1.5 million tons, in line with our estimate of 1.9 million tons. Gross margin fell sharply to $2 per ton from $111 per ton, as higher raw material costs overwhelmed the benefit of better volumes. The average DAP selling price was $668 per ton versus $623 per ton in the year-ago quarter.

The Potash segment delivered net sales of $667 million, up from $570 million a year ago. Sales volumes were 2.2 million tons compared with 2.1 million tons in the prior-year period. The figure beat our estimate of 2.1 million tons. Gross margin improved to $88 per ton from $80 per ton. Higher realized prices more than offset a higher cost environment. The average MOP selling price rose to $265 per ton from $223 per ton.

Mosaic Fertilizantes posted net sales of $937 million, essentially flat with $934 million a year ago. Sales volumes declined to 1.6 million tons from 1.8 million tons, while gross margin compressed to $22 per ton from $69 per ton. The average finished product selling price increased to $527 per ton from $452 per ton. The company said the decision to idle operations at Araxa and Patrocinio resulted in charges totaling $442 million, which drove the reported loss in the quarter. The ongoing credit constraints in Brazil were also flagged as a headwind to distribution margins.

MOS' Financials

Mosaic ended the quarter with cash and cash equivalents of $281.8 million, compared with $276.6 million at the end of 2025. Long-term debt (net of current maturities) was $4,271.1 million versus $4,250.9 million at the end of 2025.

Cash flow from operating activities was $104.2 million in the first quarter, up from $42.9 million a year ago, aided by improved working capital dynamics. Capital expenditures were $356.8 million, and free cash flow was negative $252.6 million, consistent with typical first-quarter seasonality.

Mosaic paid a regular dividend of 22 cents per share in the quarter.

MOS 2026 Outlook

For 2026, Mosaic reduced capital expenditure guidance by $250 million to $1.25 billion and maintained its potash production outlook of about 9 million tons. For the second quarter, phosphate sales volumes are expected to be 1.4 to 1.7 million tons with DAP prices of $760 to $780 per ton, while potash sales volumes are projected to be 1.9 to 2.1 million tons with MOP prices of $260 to $280 per ton. Management also reaffirmed key annual guideposts, including SG&A expense of $520 to $540 million, net interest expense of $200 to $220 million, and cash taxes of $275 to $325 million.

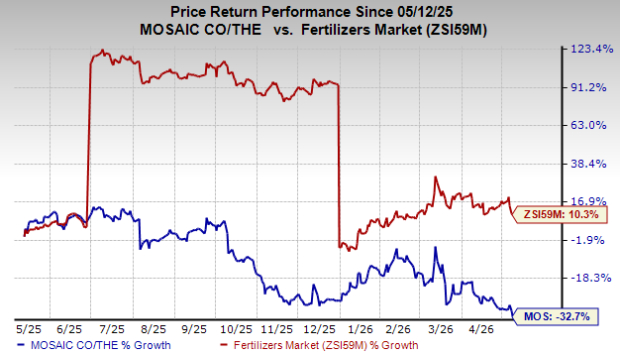

MOS’ Price Performance

Mosaic’s shares have lost 32.7% in the past year compared with the Zacks Fertilizers industry’s 10.3% rise.

Image Source: Zacks Investment Research

MOS’s Zacks Rank & Key Picks

MOS currently carries a Zacks Rank #3 (Hold).

Some better-ranked stocks in the basic materials space are Idaho Strategic Resources, Inc. IDR, NioCorp Developments Ltd. NB and Hawkins, Inc. HWKN.

Idaho is expected to report first-quarter 2026 results on May 14. The Zacks Consensus Estimate for earnings is pegged at 43 cents per share, indicating 258.33% year-over-year growth. IDR sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

NioCorp is expected to report third-quarter fiscal 2026 results on May 14. The consensus estimate for NB’s loss per share is pegged at 2 cents, indicating 83.33% year-over-year growth. NB presently carries a Zacks Rank #1.

Hawkins is scheduled to report fiscal fourth-quarter 2026 results on May 13. The Zacks Consensus Estimate for HWKN’s first-quarter earnings per share is pegged at 77 cents. HWKN carries a Zacks Rank #2 (Buy) at present.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).