Olin Posts Narrower-Than-Expected Q1 Loss, Revenues Down Y/Y

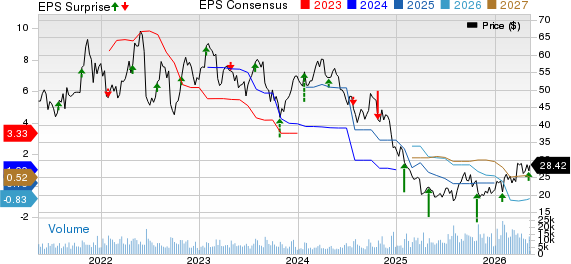

Olin Corporation OLN reported a first-quarter 2026 adjusted loss of 65 cents per share, narrower than the Zacks Consensus Estimate of a loss of 67 cents, delivering a 3% earnings surprise.

On a reported basis, the company posted a net loss of $83 million, or 73 cents, versus year-ago net income of $1.4 million, or a penny per share.

Sales were $1,583 million, down 3.7% year over year but ahead of the consensus estimate of $1,565.6 million by 1.1%.

Adjusted EBITDA came in at $86.2 million, with results reflecting weaker Chemicals conditions that were partially offset by stronger Winchester sales.

Olin Corporation Price, Consensus and EPS Surprise

Olin Corporation price-consensus-eps-surprise-chart | Olin Corporation Quote

OLN's Segmental Review

Chlor Alkali Products and Vinyls sales were $756.9 million, down from $924.5 million in the year-ago quarter. The reported figure missed the consensus estimate of $799 million. Olin attributed the decline to lower volumes and pricing, with volumes pressured by reduced trading activity tied to the Blue Water Alliance joint venture, which concluded operations at the end of 2025.

Epoxy sales increased to $355.6 million from $331.7 million, supported by higher volumes. The metric beat the consensus estimate of $349 million. Segment loss was lower due to lower operating costs, even as product margins were slightly down year over year.

Winchester sales rose to $470.5 million from $388 million, driven by higher military project revenues and military sales, along with higher commercial ammunition sales. It outpaced the consensus estimate of $408 million.

OLN's Financials

Olin ended the quarter with cash and cash equivalents of $192.2 million. Net debt was approximately $2.8 billion. Net cash used in operating activities was $48.6 million in the first quarter, compared with $86 million used in the prior-year quarter. Olin paid $22.8 million in dividends and did not repurchase common stock during the quarter.

OLN's Outlook

Management expects sequential improvement in Chemicals in the second quarter, driven by seasonally stronger demand and improved pricing, particularly for ethylene dichloride, caustic soda and epoxy resins. In Winchester, the company sees improving commercial and military demand supporting sequential earnings growth, alongside pricing measures aimed at offsetting raw material inflation.

Olin guided second-quarter 2026 adjusted EBITDA to a range of $160 million to $200 million. The company also noted that the Iran conflict began impacting trade flows late in the first quarter and lifted raw material and feedstock costs, with global supply shortages potentially persisting into the second quarter and beyond.

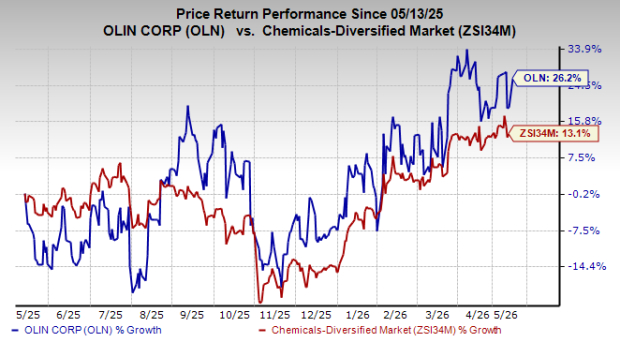

Olin’s Price Performance

Shares of Olin have gained 26.2% in the past year, compared with 13.1% rise of the industry.

Image Source: Zacks Investment Research

OLN’s Zacks Rank & Key Picks

OLN currently carries a Zacks Rank #3 (Hold).

Some better-ranked stocks in the basic materials space are Idaho Strategic Resources, Inc. IDR, NioCorp Developments Ltd. NB and Hawkins, Inc. HWKN.

Idaho is expected to report first-quarter 2026 results on May 14. The Zacks Consensus Estimate for earnings is pegged at 43 cents per share, indicating 258.33% year-over-year growth. IDR sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

NioCorp is expected to report third-quarter fiscal 2026 results on May 14. The consensus estimate for NB’s loss per share is pegged at 2 cents, indicating 83.33% year-over-year growth. NB presently flaunts a Zacks Rank #1.

Hawkins is scheduled to report fiscal fourth-quarter 2026 results on May 13. The Zacks Consensus Estimate for HWKN’s first-quarter earnings per share is pegged at 77 cents. HWKN carries a Zacks Rank #2 (Buy) at present.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).