Robinhood's Convertible Debt Play: Dilution Risk, Growth Upside

Robinhood Markets’ HOOD $2 billion convertible debt offering looks less like a distress signal and more like an opportunistic balance sheet move. The company priced 0.00% convertible senior notes due 2029, giving it a sizeable capital cushion without adding regular interest expense. That matters because the company is expanding across higher-growth areas, including crypto, prediction markets, retirement, wealth management and institutional products.

The proceeds give Robinhood three financial advantages. First, roughly $290 million will be used for share repurchases, helping offset immediate dilution concerns and supporting per-share metrics. Second, $112 million will fund capped call transactions, which are designed to reduce potential dilution if the notes convert, up to a cap price of about $237.85 per share. Third, the remaining proceeds can be deployed toward organic investments, acquisitions and capital expenditures.

The timing is important. Robinhood entered 2026 with strong operating momentum. In the first quarter, revenues rose 15% year over year to $1.07 billion, net income reached $346 million and adjusted EBITDA was $534 million. As of May 31, 2026, platform assets climbed 48% year over year to $377 billion, while event-contract trading hit 3.9 billion contracts in May.

For investors, the key risk is future dilution if Robinhood’s stock rallies sharply above the conversion threshold. However, the 65% conversion premium, buybacks and capped calls soften that concern. With no regular coupon, the notes preserve cash while giving HOOD dry powder to fund expansion. If management deploys the capital effectively, this debt play could support revenue diversification, operating scale and long-term earnings power.

Robinhood’s Peers Diversifying Their Businesses

Two close peers of HOOD are Charles SchwabSCHW and Interactive Brokers GroupIBKR.

Schwab is diversifying beyond brokerage into wealth management, advisory, banking, lending, retirement and asset management. Schwab’s fee-based assets, net interest income and broader financial services reduce commission dependence, support steadier revenues and deepen client relationships.

Interactive Brokers is diversifying through global market access, high-yield cash balances, securities lending, institutional services, retirement accounts and advisor solutions. Interactive Brokers’ interest income, international reach and technology platform reduce trading-commission reliance while supporting scalable growth.

HOOD’s Price Performance, Valuation & Estimate Analysis

Over the past three months, Robinhood’s shares have soared 53%, outperforming the industry’s growth of 17.4%.

Image Source: Zacks Investment Research

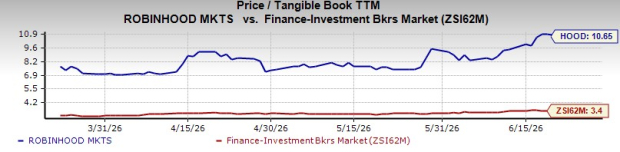

HOOD’s shares are currently trading at a premium to the industry. The company has a 12-month trailing price-to-tangible book (P/TB) of 10.65X compared with the industry average of 3.40X.

Image Source: Zacks Investment Research

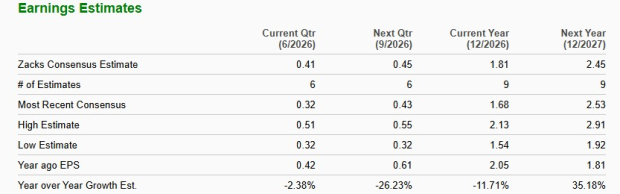

The Zacks Consensus Estimate for Robinhood’s 2026 earnings suggests a year-over-year decline of 11.7%. The trend is likely to reverse next year, with earnings expected to jump 352%. In the past week, earnings estimates for 2026 and 2027 have remained unchanged at $1.81 and $2.45 per share, respectively.

Image Source: Zacks Investment Research

HOOD currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).