Constellation Brands to Report Q4 Earnings: Can It Surprise Investors?

Constellation Brands, Inc. STZ is scheduled to release fourth-quarter fiscal 2026 results on April 8, 2026. The alcoholic beverage bigwig is expected to have recorded declines in its top and bottom lines in the to-be-reported quarter.

The Zacks Consensus Estimate for the company’s fiscal fourth-quarter earnings is pegged at $1.73 per share, indicating a 34.2% decline from the year-ago quarter’s actual. The consensus mark has moved up by a penny in the past 30 days. The consensus estimate for revenues is pegged at $1.89 billion, suggesting a 12.6% decline from the prior-year quarter’s reported figure.

The Zacks Consensus Estimate for the company’s fiscal 2026 earnings is pegged at $11.64 per share, indicating a 15.5% decline from the year-ago quarter’s actual. The consensus mark has been unchanged in the past 30 days. The consensus estimate for revenues is pegged at $9.1 billion, suggesting a 10.8% decline from the prior-year quarter’s reported figure.

In the last reported quarter, the alcohol behemoth delivered an earnings surprise of 15.04%. Its bottom line beat estimates by 8.6%, on average, in the trailing four quarters.

Constellation Brands Inc Price and EPS Surprise

Constellation Brands Inc price-eps-surprise | Constellation Brands Inc Quote

What the Zacks Model Says for STZ Stock

Our proven model does not conclusively predict an earnings beat for Constellation Brands this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. But that is not the case here. You can uncover the best stocks before they are reported with our Earnings ESP Filter.

Constellation Brands currently has an Earnings ESP of -1.59% and a Zacks Rank #3.

Key Factors to Note Before STZ’s Q4 Results

Constellation Brands’ fourth-quarter fiscal 2026 results are expected to reflect the impacts of the continued sluggishness in the wine and spirits segment due to a decline in shipment volumes. The soft volumes are expected to reflect the impacts of the SVEDKA divestiture and the 2025 Wine divestitures, as well as changes in financial and volume with respect to distributor contractual obligations.

On the last reported quarter’s earnings call, management expects this softness to continue ahead. It expects organic net sales for the wine and spirits segment to decline 17-20% in fiscal 2026, and operating income to decrease 97-100%.

High packaging and raw material costs from continued inflationary pressures, as well as increased depreciation and operating costs from brewery capacity expansions, are likely to have been concerning. This is expected to have impacted the operating income in the beer, and wine and spirits businesses.

For fiscal 2026, management continues to project an enterprise organic net sales decrease of 4-6%. Beer segment net sales are likely to decline 2-4%. The company expects operating income to fall 7-9% for the beer segment. The company continues to anticipate comparable EPS of $11.30-$11.60 for fiscal 2026. STZ expects fiscal 2026 EPS to be $9.72-$10.02.

However, Constellation Brands is on track with its plans to invest in the next phase of capacity expansion in Mexico. This will help meet the potential demand for the high-end Mexican beer portfolio, including the Alternative Beverage Alcohol sub-space, which includes hard seltzers. The company has been on track to support the industry-leading beer business, reset its cost base and redefine the portfolio. It has been focused on boosting distribution gains and innovation.

Constellation Brands' premiumization strategy is proving successful, as demonstrated by accelerated growth of its Power Brands. The wine and spirits business has been transitioning its portfolio toward higher-end brands that align better with consumer-led premiumization trends. Key growth drivers included the company's high-end Power Brands, such as The Prisoner Brand Family, Kim Crawford and Meiomi.

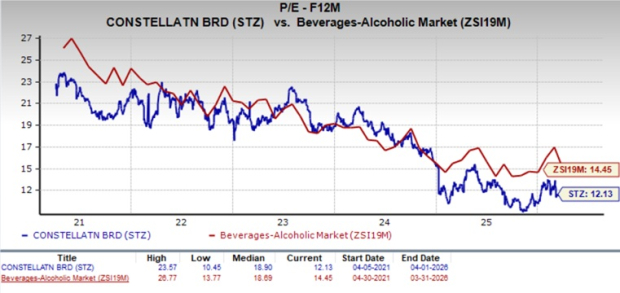

STZ Stock’s Valuation Picture

From a valuation perspective, Constellation Brands offers an attractive opportunity, trading at a discount relative to historical and industry benchmarks. With a forward 12-month price-to-earnings ratio of 12.13X, which is below the five-year high of 23.57X and the Beverages - Alcohol industry’s average of 14.45X, the stock offers compelling value for investors seeking exposure to the alcohol beverages space.

Image Source: Zacks Investment Research

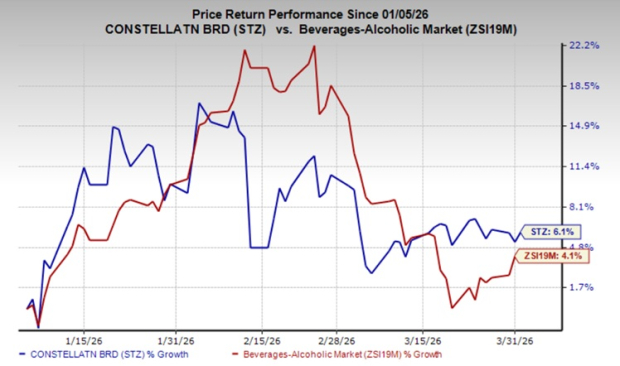

The recent market movements show that STZ shares gained 6.1% in the past three months compared with the industry's 4.1% growth.

Image Source: Zacks Investment Research

Stocks With the Favorable Combination

Here are some companies, which, according to our model, have the right combination of elements to post an earnings beat this time around:

PepsiCo Inc.PEP presently has an Earnings ESP of +0.03% and a Zacks Rank #3. The company is expected to register top and bottom-line growth when it reports first-quarter 2026 results. The Zacks Consensus Estimate for quarterly revenues is pegged at $18.95 billion, which indicates a rise of 5.7% from the figure reported in the prior-year quarter. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for quarterly earnings has been unchanged in the past 30 days. The consensus mark for PepsiCo’s earnings indicates growth of 4.7% from the year-ago quarter’s reported number. PEP delivered an earnings surprise of 1.2%, on average, in the trailing four quarters.

The Coca-Cola Company KO currently has an Earnings ESP of +0.54% and a Zacks Rank #3. The Zacks Consensus Estimate for first-quarter 2026 EPS is pegged at 81 cents, which implies an increase of 11% from the year-ago quarter’s actual. The consensus mark has been unchanged in the past 30 days.

The consensus mark for Coca-Cola’s quarterly revenues is pegged at $12.3billion, which indicates growth of 10.6% from the figure reported in the prior-year quarter. KO delivered a trailing four-quarter earnings surprise of 3.6%, on average.

Altria GroupMO currently has an Earnings ESP of +1.64% and a Zacks Rank #3. The company is expected to register growth in its top and bottom lines when it reports first-quarter 2026 results. The Zacks Consensus Estimate for MO’s quarterly earnings has moved up by a penny in the past 30 days to $1.25 per share. The consensus estimate for earnings indicates 1.6% growth from the year-ago quarter's number.

The Zacks Consensus Estimate for Altria Group’s quarterly revenues is pegged at $4.6 billion, implying a rise of 1% from the figure reported in the prior-year quarter. MO delivered an earnings surprise of 2.5%, on average, in the trailing four quarters.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

SeeThis article originally published on Zacks Investment Research (zacks.com).