Essent Group Stock Outlook Hinges on Capital, Credit and Rates

Essent Group ESNT sits at a key point in mortgage credit, housing affordability and capital discipline. Its core question is whether balance-sheet protection can offset a slower origination market.

The setup is balanced. Stable mortgage insurance economics, broader reinsurance activity and title optionality support the case, while higher rates and rising reserves temper near-term acceleration.

How Essent Makes Money

Essent serves the U.S. housing finance market through private mortgage insurance, third-party mortgage credit reinsurance, and title insurance and settlement services. Mortgage insurance remains the main engine, contributing about $1.1 billion of 2025 revenues.

The business supports low-down-payment lending by helping eligible loans move into the secondary market. Mortgage insurance in force was $248.4 billion at year-end 2025. MGIC Investment Corporation MTG and Radian Group RDN frame the same private mortgage insurance cycle, making them useful peers for investors tracking low-down-payment credit demand.

ESNT’s Core Unit Economics Stay Firm

Persistency is central because policies stay active longer when borrowers hold attractive mortgage rates. Essent’s persistency was 84.7% in the first quarter of 2026, supported by an in-force book with nearly half of note rates at or below 5.5%.

Pricing has also held steady. The base mortgage insurance premium rate was 41 basis points throughout 2025 and again in the first quarter of 2026, while the net premium rate was 35 basis points. The mortgage insurance combined ratio improved to 34.8% from 42% sequentially.

Essent’s Capital Cushion Supports Returns

Capital strength matters for a housing-linked insurer because credit losses can rise as books season. Essent ended the first quarter of 2026 with Private Mortgage Insurer Eligibility Requirements sufficiency of 174%, $1.6 billion of excess available assets and a risk-to-capital ratio of 8.6:1.

The company had about $1.1 billion of holding-company liquidity, an undrawn $500 million revolver and reinsurance protection on 96% of insurance in force. It raised dividends in each of the past six years and repurchased 3.5 million shares for $214 million from the start of 2026 through April 30.

ESNT Faces a Tougher Housing Backdrop

The operating environment is not broken, but it is limiting volume growth. Elevated mortgage rates and strained affordability continue to pressure purchase and refinance activity, weighing on new insurance written and title volumes.

Credit is normalizing as older books season. Essent’s default rate rose to 2.54% in the first quarter of 2026 from 2.12% in the second quarter of 2025. Loss reserves increased to $486 million from $447 million sequentially, while muted mortgage reinsurance demand limits Essent Re’s near-term growth.

What Could Change Essent’s Narrative

A stronger mortgage industry recovery would be the clearest swing factor. Faster origination improvement could lift new business, support title activity and give Essent more room to grow without leaning only on persistency.

Diversification also bears watching. Essent Re is preparing to expand into property and casualty reinsurance in 2026, though the near-term earnings impact is expected to be immaterial. Higher investment income and better title scale could become more meaningful if housing activity improves.

How ESNT’s Ratings Frame the Setup

The bottom line is that ESNT offers a capital-backed, value-oriented setup rather than a clean growth acceleration story. Its Zacks Rank #2 (Buy) points to supportive short-term estimate sentiment over the next one to three months. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

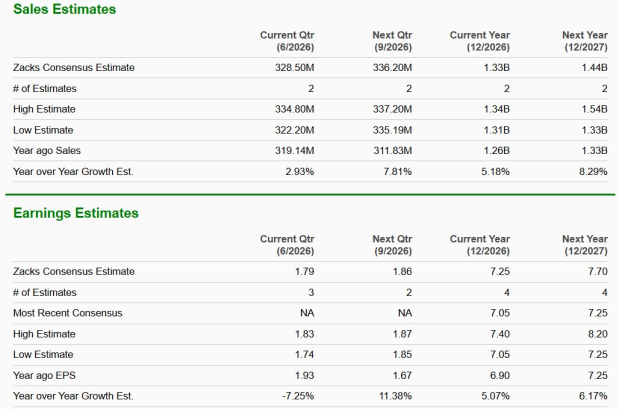

The consensus estimate for 2026 and 2027 earnings witnessed no movement in the last 30 days.

Image Source: Zacks Investment Research

The consensus estimate for ESNT 2026 and 2027 revenues and earnings indicates year-over-year increases.

Image Source: Zacks Investment Research

The Style Scores are mixed. ESNT has a Value Score of A, but a Growth Score of F, Momentum Score of D and VGM Score of D. That fits a stock with valuation support and solid fundamentals, but less obvious near-term upside acceleration than investors typically seek from stronger growth and momentum profiles.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).