Chipotle Gears Up for Q1 Earnings: Buy Now or Wait It Out?

Chipotle Mexican Grill, Inc.CMG is slated to release first-quarter 2026 results on April 29, after the closing bell.

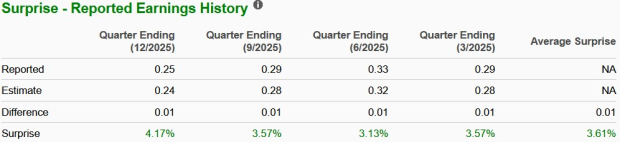

In the last reported quarter, the company’s earnings beat the Zacks Consensus Estimate by 4.2%. CMG’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 3.6%, as shown in the chart below.

Image Source: Zacks Investment Research

CMG’s Q1 Estimate Revisions

The Zacks Consensus Estimate for first-quarter earnings per share (EPS) has been unchanged at 24 cents in the past 30 days. The projected figure indicates a 17.2% decline from the year-ago reported EPS of 29 cents. The consensus mark for revenues is pegged at $3.08 billion, implying 7% year-over-year growth.

What the Zacks Model Unveils for CMG

Our proven model conclusively predicts an earnings beat for CMG this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. This is exactly the case here.

CMG’s Earnings ESP: Chipotle currently has an Earnings ESP of +1.11%. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Zacks Rank of CMG: The company carries a Zacks Rank #3 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Factors Influencing CMG’s Q1 Performance

Chipotle’s top-line performance in first-quarter 2026 is likely to have benefited from menu innovation and compelling product launches. The company introduced a high-protein menu aligned with consumer demand for healthier and protein-rich food choices. This initiative appears to have driven higher add-on purchases, such as extra protein, while also boosting digital engagement during promotions. In addition, limited-time offers, including the return of popular items, are likely to have attracted new customers and encouraged repeat visits, thereby supporting transaction growth.

Another important contributor is likely to have been strong marketing efforts and refined brand positioning. Chipotle increased the marketing spend to enhance visibility and reinforce its value proposition centered on quality ingredients and differentiated offerings. Targeted campaigns, including those tied to social engagement and key consumption occasions, are likely to have resonated well with younger and digitally active consumers. These initiatives, backed by deeper consumer insights, are expected to have driven traffic and strengthened overall sales momentum.

The company’s loyalty program growth and digital ecosystem enhancements also appear to have supported the top line. With a large and expanding base of active rewards members, Chipotle has been leveraging personalization and gamification to increase engagement and spending. The ongoing efforts to improve the in-store and digital experience, along with a planned relaunch of the rewards program, are likely to have boosted both frequency and average ticket size. Additionally, improved throughput from operational upgrades and continued restaurant expansion might have further aided revenue growth by enhancing service speed and capacity.

Our model predicts Food and Beverage and Delivery Service revenues to increase 6.5% and down 0.8% year over year, respectively.

Margins in the first quarter of 2026 are likely to have been pressured by rising input and operating costs, along with strategic investments. Inflation in key ingredients such as beef, avocados and cooking oils, along with wage increases, is likely to have driven the higher cost of sales and labor expenses. At the same time, the company adopted a measured pricing strategy, with price hikes not fully offsetting inflation, creating margin pressure.

Increased marketing spends, higher delivery and utility costs, and continued investments in technology and operations are also likely to have weighed on profitability during the quarter. Our models predict restaurant operating costs to increase 11.6% year over year to $2,673.1 million.

Price Performance & Valuation of CMG

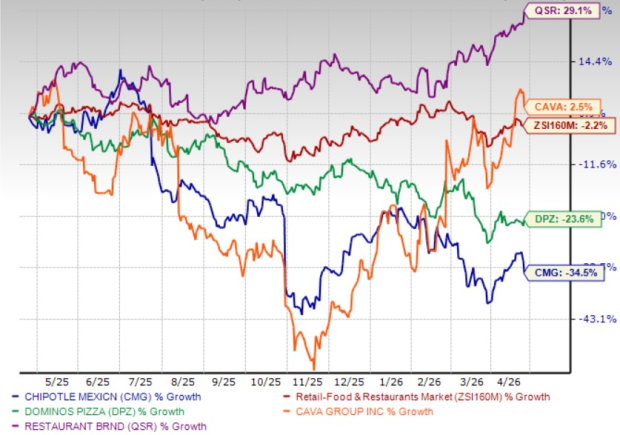

CMG stock has declined 34.5% over the past year compared with the industry’s decrease of 2.2%. In the same time frame, shares of other industry players like Domino’s Pizza, Inc.DPZ, CAVA Group, Inc.CAVA and Restaurant Brands International Inc.QSR have declined 23.6% and gained 2.5% and 29.1%, respectively.

Price Performance

Image Source: Zacks Investment Research

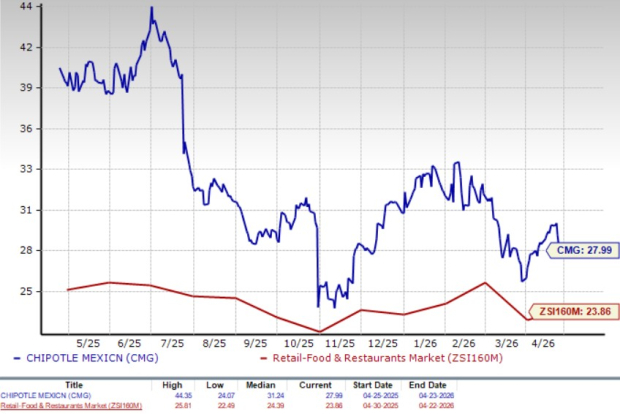

Analysts have expressed concerns that CMG stock is overvalued. The company is currently valued at a premium compared with its industry on a forward 12-month P/E basis. Its forward 12-month price-to-earnings ratio stands at 27.99, higher than the industry average.

P/E (F12M)

Image Source: Zacks Investment Research

Investment Thoughts for CMG

Chipotle presents a mixed near-term picture, with solid top-line drivers like menu innovation, marketing strength and digital engagement being offset by cost pressures and ongoing investments. While the company’s brand strength and long-term growth strategy remain intact, profitability is likely to stay under pressure due to inflation and a cautious pricing approach. At the same time, the stock’s premium valuation limits the scope for immediate upside. Given this combination, existing investors may consider holding the stock to benefit from its long-term potential, while new investors may prefer to wait for a more attractive entry point and clearer signs of margin improvement.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>This article originally published on Zacks Investment Research (zacks.com).