Roblox Stock Gains 32% in a Month: Should Investors Buy, Sell or Hold?

Shares of Roblox CorporationRBLX have rallied 31.9% in the past month, outperforming the Zacks Gaming industry’s 6.2% rise and the S&P 500’s 2% growth.

RBLX shares have gained momentum, supported by improving platform-engagement sentiment and easing concerns over safety-related friction. A recent report highlighted a meaningful pickup in weekend user engagement, supported by seasonal summer activity, Russia re-entry and the popularity of Grow a Garden 2. These factors, along with progress on Roblox Kids and Roblox Select accounts, AI-enabled creation tools and enhanced developer incentives, likely supported the recent appreciation in the stock.

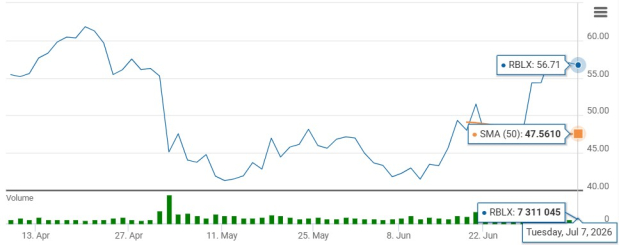

RBLX One-Month Price Performance

Image Source: Zacks Investment Research

From a technical perspective, RBLX is currently trading above its 50-day moving average, indicating solid upward momentum and price stability.

RBLX Stock Trades Above 50-Day Moving Average

Image Source: Zacks Investment Research

As of yesterday, Roblox stock is trading 62.3% below its 52-week high of $150.59. So, should investors pour more capital into RBLX now? Let us take a closer look.

Key Drivers Supporting Roblox's Performance

Roblox’s engagement profile remains a key pillar of its growth story. In the first quarter of 2026, daily active users increased 35% year over year to 132 million, while hours engaged rose 43% to 31 billion. International markets continued to provide meaningful momentum, with DAUs outside the United States and Canada increasing 40%. Japan and India stood out, with DAUs rising 96% and 84%, respectively. These trends indicate that Roblox’s global expansion runway remains substantial, even as safety-related platform changes create some near-term friction in user growth.

The company’s creator ecosystem also remains a long-term competitive advantage. Games outside the top 10 delivered 43% growth in engagement and 41% growth in spending, accounting for 65% of total spending growth in the quarter. This reflects healthier content diversity and reduces Roblox’s dependence on a limited number of viral titles. The company is also refining its discovery algorithms to favor high-quality experiences with stronger long-term retention, rather than prioritizing near-term monetization alone.

AI-led creation tools add another layer to Roblox’s growth narrative. Nearly half of the platform’s top 1,000 creators now use Roblox Assistant or model context protocol tools to shorten development timelines. The company is also expanding agentic capabilities within Roblox Studio, along with mesh generation, procedural model creation and NPC testing agents. These initiatives are designed to help smaller creator teams build richer experiences more efficiently, strengthening Roblox’s content pipeline and supporting long-term platform engagement.

The 18-and-up cohort also represents a meaningful monetization opportunity. Roblox is increasing creator payouts for spending by age-checked U.S. users aged 18 and above, with the payout rate rising to as much as 37.8% from 26.6%. Since U.S. users above 18 monetize more than 50% higher than under-18 users, the higher payout could give developers a stronger incentive to build content for older users and support Roblox’s long-term monetization runway.

RBLX’s Concerns: Safety Friction & Margin Pressure

Despite strong first-quarter growth, Roblox faces several near-term challenges that could slow its momentum in 2026. The company sharply reduced its full-year bookings growth outlook to 8-12%, down from its prior 22-26% projection. The revised outlook is largely tied to safety-related friction, including the global rollout of age checks, weaker communication engagement and softer top-of-funnel user growth. Management expects DAUs to contract sequentially from the first quarter to the second quarter before returning to growth in the third quarter.

Safety initiatives remain a key pressure point. Roblox introduced age checks to access chat globally and restricted adults from communicating with users under 16. While these measures support long-term platform trust and safety, they have reduced the number of users able to communicate on the platform. Management noted that weaker chat density can affect both age-checked and non-age-checked users, creating friction in engagement and organic user acquisition.

The company is also dealing with weaker app store dynamics. Roblox said lower communication activity, discovery systems that had been more biased toward monetization and reduced organic sign-ups likely pressured app store ratings. This creates a near-term growth hurdle, particularly as new-user acquisition has been the main area of weakness, even though retention, engagement and monetization have remained solid.

Margin pressure is another concern. The lower bookings outlook is expected to weigh on profitability through fixed-cost deleveraging. In addition, roughly one-fourth of the margin reduction versus prior guidance is tied to incremental investments in artificial intelligence and the higher DevEx rate for age-checked 18-and-up users in the United States. These initiatives could strengthen Roblox’s long-term creator ecosystem, but they add spending pressure in the near term.

Roblox Stock vs. Digital Entertainment Peers: How It Stacks Up

Roblox operates in a competitive gaming and digital-entertainment landscape alongside Take-Two Interactive Software, Inc. TTWO, Unity Software Inc. U and DraftKings Inc.DKNG, each with a distinct growth model.

Take-Two benefits from a deep portfolio of owned franchises, including Grand Theft Auto, NBA 2K and Red Dead Redemption, with Grand Theft Auto VI expected to serve as a major growth catalyst. Unity Software is strengthening its position in game-creation infrastructure through Vector, Unity AI and broader workflow tools for developers. DraftKings, while less directly comparable, is expanding its interactive consumer platform across Sportsbook, iGaming and Predictions.

For Roblox, the growth outlook remains tied to platform engagement, creator activity, AI-enabled development tools and the expanding 18-and-up monetization opportunity. Its user-generated content model supports recurring engagement without relying on a traditional release cycle. Take-Two offers stronger franchise-led visibility, Unity Software is advancing rapidly in AI-powered creator technology, and DraftKings continues to show disciplined execution in digital entertainment. Still, Roblox’s global scale, international reach and expanding creator ecosystem support a favorable long-term profile, even as competition keeps the execution bar high.

RBLX Stock Valuation Insights

Over the past 60 days, the Zacks Consensus Estimate for RBLX’s 2026 loss per share has narrowed 0.7% in the past 60 days. Over the same time frame, earnings estimates for industry players, including DraftKings and Unity Software, have increased 0.9% and 5.1%, respectively, while earnings estimates for TTWO have declined 15.4%.

RBLX’s Earnings Estimate Trend

Image Source: Zacks Investment Research

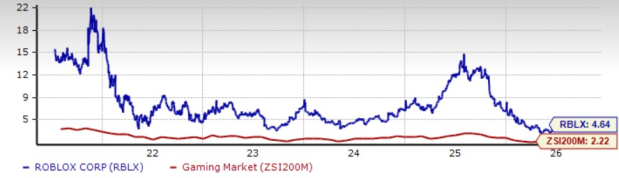

Roblox stock trades at a premium. RBLX’s forward 12-month P/S multiple of 4.64X is above the industry average of 2.22X. Among peers, DraftKings, Unity Software and TTWO trade at forward P/S multiples of 1.83X, 5.73X and 5.49X, respectively.

RBLX’s P/S Ratio (Forward 12-Month) vs. Industry

Image Source: Zacks Investment Research

Our Thoughts on RBLX Stock

Roblox remains an interesting long-term platform story within the gaming and digital-entertainment space. The company is benefiting from strong engagement growth, continued international expansion, a diversified creator ecosystem and improving sentiment around its user-generated content model.

AI-led creation tools provide RBLX with levers to strengthen content development, improve creator productivity and support richer platform experiences. The expanding 18-and-up opportunity, higher creator incentives and improving discovery algorithms also support the long-term monetization narrative.

However, the recent rally appears to reflect stronger engagement sentiment and renewed investor confidence, while near-term fundamentals still face some pressure. Safety-related platform changes have affected communication activity and organic sign-ups, though the company’s bookings outlook remains modest. Higher AI investments and increased developer payouts could also weigh on margins in the near term.

Given these mixed factors, the sharp one-month gain does not necessarily signal that Roblox’s growth trajectory is fully derisked. While the company’s global scale, creator ecosystem and AI initiatives remain noteworthy, the stock’s premium valuation calls for a more measured approach.

For now, RBLX’s Zacks Rank #3 (Hold) appears appropriate. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).