Should You Buy, Sell or Hold FCX Stock Ahead of Q1 Earnings?

Freeport-McMoRan Inc. FCX is slated to report first-quarter 2026 results before the opening bell on April 23. While higher unit costs and weaker volumes are likely to have impacted FCX’s performance, it is expected to have benefited from favorable copper prices.

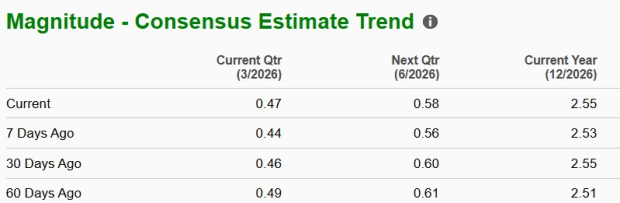

The Zacks Consensus Estimate for first-quarter earnings has been revised lower in the past 60 days. The consensus estimate for earnings is pegged at 47 cents per share, suggesting a 95.8% year-over-year rise. The Zacks Consensus Estimate for revenues currently stands at $5.61 billion, indicating a 2% decline on a year-over-year basis.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

FCX beat the Zacks Consensus Estimate for earnings in three of the last four quarters and reported in-line results once. It has a trailing four-quarter earnings surprise of 26.8% on average.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Q1 Earnings Whispers for FCX Stock

Our proven model does not conclusively predict an earnings beat for FCX this season. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. But that’s not the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

FCX has an Earnings ESP of -0.86% and a Zacks Rank #3. You can see the complete list of today’s Zacks #1 Rank stocks here.

Factors Shaping FCX’s Q1 Results

Freeport’s first-quarter results are expected to reflect favorable copper prices. Copper prices started 2026 on a strong note, underpinned by robust demand from China and the United States. Structural tailwinds, including electric vehicles (EVs), renewable energy projects, data center growth and grid modernization, continue to boost copper consumption. Worries about tightening supply amid rising EV and infrastructure demand also supported the red metal.

Supply risks increased amid concerns over lower output and potential disruptions at major global mining operations. These factors led to prices surging to roughly $6.4 per pound in late January. Prices of the red metal were mostly volatile during February, largely trading near $6 per pound.

Copper prices came under pressure last month amid concerns about the impact of surging oil prices on the global economy due to the war in the Middle East, dragging down prices to a three-month low of around $5.3 per pound in late March. Prices have rebounded since then on hopes of a de-escalation in the Iran war and are currently hovering around $6 per pound.

Our estimate for the first-quarter average realized copper price for FCX is $5.70 per pound, which indicates a year-over-year rise of 28.3%.

FCX’s results are likely to be unfavorably impacted by lower sales volumes due to the Grasberg mine incident. The company’s outlook for copper sales volumes for the first quarter assumes minimal contribution from its Indonesian operations due to the mine incident. FCX expects copper sales volumes of 640 million pounds, indicating a 10% sequential and 27% year-over-year decline. The company has issued weaker guidance for gold sales volume of 60,000 ounces, suggesting sequential and year-over-year decreases. Lower sales volumes are expected to weigh on its top line.

Higher unit costs are also likely to have affected the company’s performance in the March quarter. FCX saw a sharp increase in its average unit net cash cost per pound of copper in the fourth quarter of 2025 to $2.22 from $1.40 in the prior quarter, marking a roughly 59% spike. It also climbed 34% year over year. Freeport's outlook for the first quarter suggests higher costs on a sequential basis. It expects unit net cash costs to rise to $2.60 per pound, while projecting a full-year average of roughly $1.75.

FCX Stock’s Price Performance and Valuation

FCX’s shares have gained 106% in a year, underperforming the Zacks Mining - Non Ferrous industry’s 117.4% rise, while topping the S&P 500’s increase of 39.2%. Its peers, Southern Copper CorporationSCCO and BHP Group LimitedBHP, have rallied 114% and 67%, respectively, over the same period.

FCX’s One-year Price Performance

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

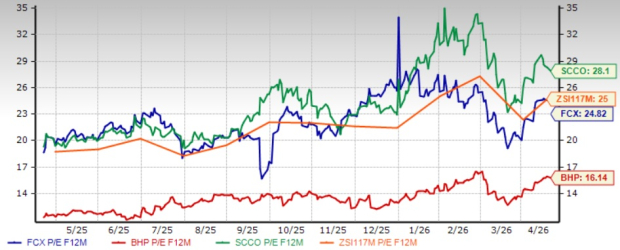

From a valuation standpoint, Freeport is currently trading at a forward 12-month earnings multiple of 24.82, a roughly 0.7% discount to the peer group average of 25X. FCX is trading at a premium to BHP Group and at a discount to Southern Copper. Freeport currently has a Value Score of C. BHP Group has a Value Score of B, while Southern Copper has a Value Score of D.

FCX’s P/E F12M Vs. Industry, SCCO & BHP

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Investment Thesis for FCX Stock

Freeport is well-placed with high-quality copper assets and remains focused on strong execution and advancing its organic growth opportunities. It is expected to gain from progress in exploration activities that will boost production capacity. FCX also has a strong liquidity position and generates substantial cash flows, which allow it to finance its growth projects, pay down debt and drive shareholder value. Backed by strong financial health, the company's dividend is perceived to be safe and reliable. The strength in copper prices should also support its profitability and drive cash flow generation.

Freeport, however, faces headwinds from higher costs, which may eat into its margins. Weaker copper volumes due to the Grasberg mine incident are also likely to weigh on its performance.

Final Thoughts: Hold Onto FCX Shares

FCX stands to benefit from the ongoing expansion initiatives that will enhance its production capacity. Its strong financial position supports continued investment in growth projects and shareholder returns. Despite these positives, softer sales volume expectations and rising unit costs remain concerns. Holding onto the FCX stock will be prudent for investors who already own it, awaiting clearer direction from the upcoming earnings release.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).