AI Memory Giant Hits All-Time High Amid Soaring Demand

AI memory giant Sandisk first came on our radar last year following its separation from Western Digital. The company was formerly Western Digital’s flash memory business that was spun off and relisted in February 2025.

A developer and manufacturer of data storage devices and solutions, Sandisk was the best performer in the S&P 500 last year and is showing continued momentum in 2026. While the broader technology sector has experienced periods of rotation and profit-taking this year, this stock has delivered exceptional performance.

Image Source: StockCharts

Despite rising dramatically since its relisting, the setup for more upside remains compelling.

Company Description

Sandisk specializes in flash-memory storage solutions such as solid-state drives (SSDs) for desktop and notebook PCs, gaming consoles, and set top boxes, as well as flash-based embedded storage products for mobile phones, tablets, and other portable devices. The company’s solutions extend to automotive, industrial, data center, and cloud applications.

Data center operators and hyperscalers continue to expand infrastructure at an unprecedented pace, driving sustained demand for NAND flash-based memory solutions. Unlike many tech names that have faced questions around near-term spending or valuation resets, Sandisk operates at the heart of the memory bottleneck that AI infrastructure has created.

High-bandwidth memory and high-density NAND are critical for both training and inference workloads, and Sandisk’s advanced technology has positioned it to capture meaningful share in data center and enterprise applications.

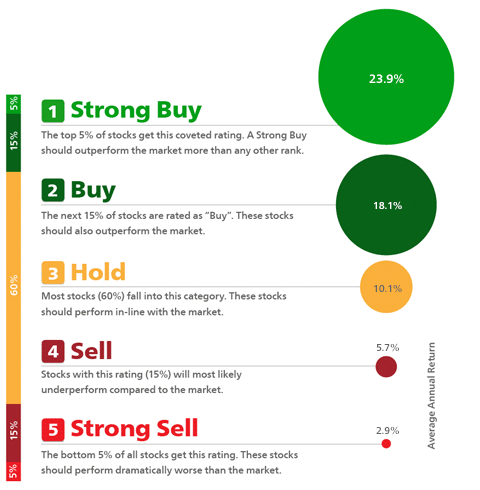

Zacks Rank System Labels Sandisk ‘Strong Buy’

If you’ve followed Zacks for a while, you know we place a big emphasis on rising earnings estimates. Why is that the case?

The Zacks Rank is a proprietary stock-rating model that uses trends in earnings estimate revisions and EPS surprises to classify stocks into five groups, ranging from “Strong Buy” to “Strong Sell”. More importantly, it allows individual investors to take advantage of trends in earnings estimate revisions, and benefit from the power of institutional investors.

Image Source: Zacks Investment Research

Stocks with rising earnings estimates have significantly outperformed the S&P 500 year after year, while stocks with falling earnings estimates have consistently underperformed the broader market.

At Zacks, we give you the tools to help identify leading stocks and outperform the market. Our Zacks Rank methodology pinpoints stocks that are witnessing positive earnings estimate revision activity, allowing investors to jump on board before an emerging rally gets underway. Our research has consistently shown that rising earnings estimates are the most powerful force impacting stock prices over time.

And that’s certainly been the case for Sandisk SNDK. The stock currently carries a Zacks Rank #1 (Strong Buy), reflecting consistent upward revisions to estimates and the company’s ability to exceed expectations. The Zacks Rank system rewards exactly this type of positive momentum, and Sandisk has been a standout in that regard. We’ll take a deeper dive into these estimates below.

Earnings Trends and Future Estimates

Sandisk has established an impressive reporting history, surpassing earnings estimates in each of the past four quarters. The company most recently delivered fiscal second-quarter earnings back in January of $6.20 per share, which marked a 75.1% surprise over the $3.54/share consensus estimate.

During the second quarter, Sandisk reported revenue of $3.03 billion, up 61% year-over-year and well above consensus expectations. Data center revenue surged 64% sequentially, driven by strong adoption among hyperscalers and AI infrastructure builders. Gross margins expanded dramatically to 51.1%, reflecting both pricing power and favorable product mix.

Image Source: Zacks Investment Research

These results were not isolated; they reflected the company’s successful transition into a higher-margin, AI-focused business following the spin-off. The AI memory powerhouse delivered a trailing four-quarter average earnings surprise of 371.3%, reflecting strong execution.

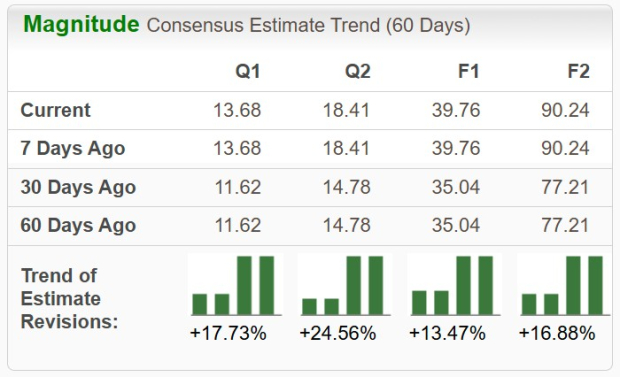

Analysts covering SNDK are in agreement and have raised their fiscal third-quarter estimates by 17.73% in the past 60 days. The Zacks Consensus Estimate now stands at $13.68/share, reflecting an astounding potential growth rate of 4,660% relative to same period in the prior year.

Image Source: Zacks Investment Research

It’s clear that analysts are modeling continued acceleration for the upcoming Q3 report. Consensus estimates call for revenue in the $4.5–$4.6 billion range, translating to a nearly 170% improvement. These figures represent enormous sequential and year-over-year growth, underscoring the momentum in Sandisk’s data center and enterprise segments.

What the Zacks Model Reveals

Our Zacks Earnings ESP (Expected Surprise Prediction) filter empowers investors by allowing them the opportunity to detect stocks that are most likely to beat consensus estimates. The Zacks Earnings ESP indicator seeks to identify companies that have recently witnessed positive earnings estimate revision activity.

The technique has proven to be quite useful for finding positive surprises. In fact, when combining a Zacks Rank #3 or better with a positive Earnings ESP, stocks produced a positive surprise 70% of the time according to our 10-year backtest.

Sandisk is currently a Zacks Rank #1 (Strong Buy) stock and boasts a +2.0% Earnings ESP. Another beat may be in the cards when the company reports its fiscal Q3 results after the market close on April 30th.

Bottom Line

The recent strength in Sandisk is rooted in a powerful combination of structural AI demand and an exceptionally tight NAND supply environment.

It’s genuinely impressive to see a company that was once part of a larger conglomerate successfully carve out its own identity and thrive. The spin-off allowed Sandisk to focus exclusively on flash memory innovation, and the results are evident in the accelerating data center revenue and margin expansion.

For investors seeking exposure to the ongoing AI infrastructure buildout, Sandisk stands out as a high-conviction idea, offering a balanced risk/reward profile with tangible earnings momentum. The stock carries a Zacks Rank #1 (Strong Buy) rating, benefitting from favorable earnings revisions, and is positioned to capture a disproportionate share of the coming storage spending wave.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).