Rocket Lab to Release Q1 Earnings: How to Approach the Stock Now?

Rocket Lab CorporationRKLB is expected to report first-quarter 2026 results on May 7, after market close.

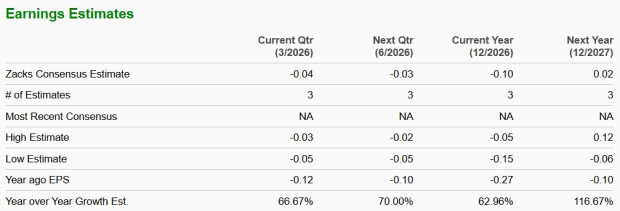

The Zacks Consensus Estimate for earnings is pegged at a loss of 4 cents per share, indicating a year-over-year rise of 66.7%. The Zacks Consensus Estimate for revenues is pinned at $191.4 million, calling for a jump of 56.2% from the year-ago reported figure.

Image Source: Zacks Investment Research

RKLB’s Earnings Surprise History

RKLB’s earnings beat the Zacks Consensus Estimate in one of the trailing four quarters and missed in three, the average surprise being 4.29%.

Image Source: Zacks Investment Research

What Our Quantitative Model Predicts for RKLB

Our proven model does not conclusively predict an earnings beat for Rocket Lab this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat, which is not the case here, as you will see below.

Earnings ESP: The company’s Earnings ESP is 0.00%. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Zacks Rank: Currently, RKLB carries a Zacks Rank #4 (Sell).

You can see the complete list of today's Zacks #1 Rank stocks here.

Recent Defense Releases

Teledyne Technologies Inc. TDY reported first-quarter 2026 adjusted earnings of $5.80 per share, which surpassed the Zacks Consensus Estimate of $5.48 by 5.9%. The bottom line also improved 17.2% from $4.95 recorded in the year-ago quarter.

Total sales were $1.56 billion, which beat the Zacks Consensus Estimate of $1.51 billion by 3.3%. The top line also jumped 7.6% from $1.45 billion reported in the year-ago quarter.

TransDigm Group IncorporatedTDG reported second-quarter fiscal 2026 adjusted earnings of $9.85 per share, which topped the Zacks Consensus Estimate of $9.32 by 5.7%. The bottom line also improved 8% from the prior-year quarter’s figure of $9.11.

Sales amounted to $2.54 billion, up 18% from $2.15 billion registered in the prior-year period. The reported figure also topped the Zacks Consensus Estimate of $2.42 billion by 4.9%.

Factors That Might Have Impacted RKLB’s Q1 Performance

Higher revenues driven by growth in the number of launch missions, together with solid revenue contributions stemming from strong bookings recorded in prior quarters, are likely to have supported the Launch Services business segment’s top line.

Solid growth in spacecraft and satellite manufacturing is likely to have contributed to revenues for the Space Systems business segment.

Rocket Lab’s first-quarter performance may have benefited from the acquisitions of Optical Support, Inc. (“OSI”) and Precision Components Limited (“PCL”), which expanded its optical payload and precision manufacturing capabilities. The deals are likely to have strengthened Rocket Lab’s position in defense, missile tracking and space systems programs. OSI may have supported higher defense-related contract opportunities, while PCL is expected to have aided Electron and Neutron production. The acquisitions are also likely to have enhanced RKLB’s vertically integrated operations and strengthened revenue generation prospects.

However, higher operating expenses related to continued investments in the Neutron program, and increased research and development spending are likely to have pressured operating margins, limiting overall earnings growth.

RKLB Stock Price Performance

Over the past three months, the stock has risen 3.9% against the industry’s decline of 6.9%.

Image Source: Zacks Investment Research

RKLB Stock Trading at a Premium

Rocket Lab is trading at a premium relative to the industry, with a forward 12-month price-to-sales of 46.09X compared with the industry average of 11.64X.

Image Source: Zacks Investment Research

RKLB Stock’s Poor ROIC

The image below shows that RKLB stock’s trailing 12-month return on invested capital (ROIC) not only lags the peer group’s average return but also reflects a negative figure. This suggests that the company's investments are not yielding sufficient returns to cover its expenses.

Image Source: Zacks Investment Research

Investment Viewpoint

Rocket Lab is gaining momentum in 2026, driven by increased hypersonic test missions and major defense contract wins. After completing three HASTE missions in 2025, it plans more in 2026 while expanding its role in U.S. defense programs through contracts like the SDA Tranche III Tracking Layer and the Missile Defense Agency’s SHIELD IDIQ.

RKLB has reiterated that SDA revenue pacing is frequently constrained by subcontractor deliveries, with optical terminal availability cited as an industry bottleneck. The company expects roughly 37% of the fourth-quarter 2025 backlog to convert within 12 months, including conservative Tranche III estimates, but supplier-driven timing can still shift revenue milestones across quarters. These constraints risk pushing recognition to later periods, increasing volatility and potentially moderating the cadence of cash inflows from large program ramp-ups.

Endnote on RKLB

Rocket Lab is benefiting from growing demand for launch services, spacecraft manufacturing and defense-related space programs, supported by strategic acquisitions and expanding deep-space capabilities. The company remains exposed to risks tied to U.S. government budget cycles, procurement delays and regulatory approvals, which may affect program execution and revenue timing. Elevated operating expenses related to Neutron development, and ongoing research and development investments continue to pressure margins and contribute to recurring losses.

Given its premium valuation, poor ROIC and continued earnings pressure, investors should avoid this stock at the moment.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>This article originally published on Zacks Investment Research (zacks.com).