Should You Buy FN Stock Post Q3 Earnings & Revenue Beat?

On May 4, Fabrinet FN, a provider of advanced optical packaging and precision optical, electromechanical and electronic manufacturing services to original equipment manufacturers of complex products, reported impressive third-quarter fiscal 2026 results (ended March 27). The high-flying tech stock reported better-than-expected earnings per share and revenues in the fiscal third quarter.

The question that naturally arises now is whether investors should take advantage of the outperformance and buy shares of the company, which is well-poised to benefit from the solid adoption of AI and the democratization of IoT, which are transforming robotics, industrial automation, transportation systems, retail and healthcare. Let us delve deeper to answer the question.

Highlights of FN’s Q3 Earnings

Fabrinet reported earnings of $3.72 per share in the third quarter of fiscal 2026 (excluding 27 cents from non-recurring items), beating the Zacks Consensus Estimate by 3.9%. The figure increased 47.6% year over year. Revenues of $1.21 billion increased 39.3% on a year-over-year basis, exceeded the guidance and surpassed the consensus mark by 1.6%.

Optical Communications revenue growth increased 35% to $888.7 million from a year ago, driven by a 55% year-over-year growth in Telecom revenues, which was fueled by strong growth in a wide range of products. Within Telecom, data center interconnect revenues surged 90% from a year ago and 38% sequentially.

In non-optical communications, revenues jumped 52% to $325.6 million year over year and 8% sequentially. The growth was driven primarily by high-performance computing revenues as FN’s customers transitioned to their latest product generation. Automotive revenues moderated in the fiscal third quarter as anticipated, with revenues decreasing modestly from the fiscal second quarter.

Fabrinet expects fourth-quarter revenues to be in the range of $1.25 billion to $1.29 billion. Adjusted earnings per share are expected to be in the range of $3.72 to $3.87. The Zacks Consensus Estimate is pegged at $3.80 on $1.26 billion in revenues.

This was the fourth successive earnings beat by FN in the last twelve months. The average beat is 2.6%.

Fabrinet Balance Sheet Strength Supports Flexibility

FN ended the fiscal third quarter with about $945.9 million in cash and short-term investments and no debt, supporting expansion plans and financial flexibility.

The company also had $169 million remaining under its share repurchase authorization, providing an additional lever during periods of volatility.

Fabrinet’s Strong Prospects Justify Premium Valuation

Fabrinet’s strong prospects, along with a debt-free balance sheet, justify a premium valuation. The company currently carries a Value Score of F.

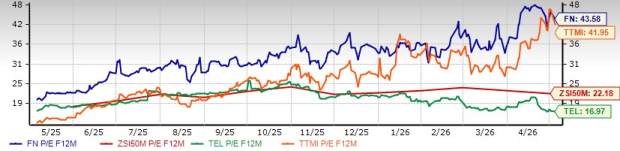

FN stock is trading at a forward 12-month price/earnings (P/E) of 43.58X compared with the Zacks Electronics - Miscellaneous Components industry’s 22.18X. The company is also trading at a premium compared with fellow industry players TE Connectivity TEL and TTM Technologies TTMI. TE Connectivity and TTM Technologies currently carry a Value Score of C and F, respectively.

FN’s P/E F12M Vs. Industry, TEL & TTMI

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

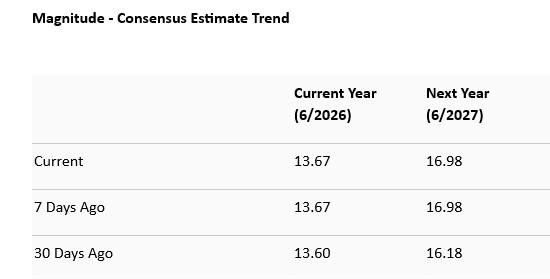

Encouraging Estimates for FN

The Zacks Consensus Estimate for FN’s fiscal 2026 and 2027 earnings per share implies 34.4% and 24.2% year-over-year upticks, respectively. Encouragingly, the company is witnessing northbound estimate revisions for the current and the next year. The consensus mark for fiscal 2026 and 2027 revenues imply 33.6% and 23.1% increases, respectively.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

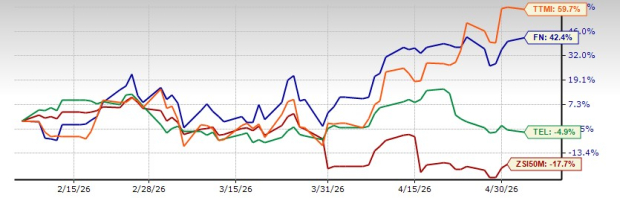

FN’s Shares Outperform Industry

Fabrinet’s shares have gained in double digits (% wise), outperforming its industry as well as TE Connectivity. TTM Technologies’ shares have performed even better.

3-Month Price Comparison

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Final Thoughts: Buy FN Stock Now

Given the positives surrounding the company, as highlighted throughout the write-up, we believe that investors should add this Zacks Rank #1 (Strong Buy) stock to their portfolios for healthy returns. The company’s current Zacks Rank supports our stance.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).