Is Winnebago Stock a Value Trap or a Contrarian Buy in 2026?

Winnebago Industries, Inc. WGO gives investors a familiar cyclical-stock puzzle. The valuation looks inexpensive, the dividend is meaningful and the company still has brands with durable recognition.

The harder question is whether those positives are enough. Earnings pressure, softer retail conditions and reduced guidance keep the value case from looking clean.

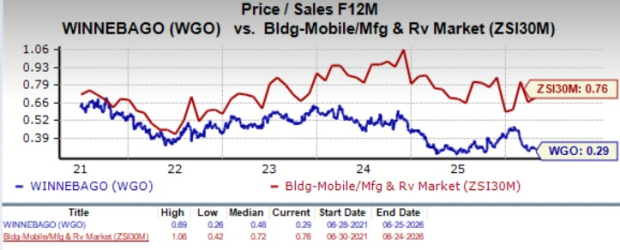

WGO Looks Cheap on Key Multiples

WGO trades at 10.82X forward 12-month earnings, below 17.5X for the Zacks sub-industry, 36.53X for the broader sector and 22.18X for the S&P 500 index. That discount is the starting point for any contrarian argument.

The stock also carries a low price-to-sales multiple of 0.29X. With the shares trading at around $30 and our price target of $32, the valuation setup points to limited embedded optimism rather than a clear rerating case.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

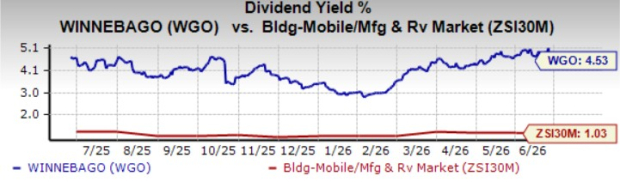

Winnebago Still Rewards Shareholders

The income profile is another reason investors may keep WGO on a watchlist. The stock’s dividend yield is 4.5%, supported by a quarterly dividend of 35 cents per share.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Winnebago returned $88.9 million to investors in fiscal 2025, including $50 million through buybacks and $38.9 million through dividends. The company has paid a quarterly dividend for 48 consecutive quarters and has raised its dividend five times over the past five years.

Why WGO Earnings Risk Has Not Cleared

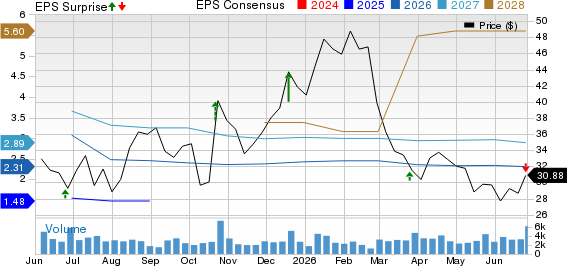

Third-quarter fiscal 2026 results weakened the bargain argument. Winnebago reported adjusted earnings of 66 cents per share and revenues of $698.7 million, below the expected 91 cents per share and $770 million in revenues.

Winnebago Industries, Inc. Price, Consensus and EPS Surprise

Winnebago Industries, Inc. price-consensus-eps-surprise-chart | Winnebago Industries, Inc. Quote

Management also lowered fiscal 2026 guidance. Consolidated revenues are now expected between $2.65 billion and $2.75 billion, while adjusted earnings are projected between $1.65 and $2 per share, down from the prior $2.10-$2.80 range.

Affordability pressure, cautious dealer ordering and macro uncertainty are still weighing on demand. THOR IndustriesTHO offers a useful peer lens because it also competes across RV categories through brands such as Airstream and Jayco, making it relevant to any assessment of RV-cycle pressure.

Winnebago’s Weak Spots Still Matter

The latest quarter showed that segment mix remains uneven. Towable RV revenues fell 26.1% year over year to $274.7 million, hurt by lower unit volume and a shift toward lower price-point models.

Marine revenues declined 8.3% to $92.4 million as lower unit volume and product mix pressured results. Both Towable RV and Marine also saw lower operating margins, with higher input costs and volume deleverage offsetting some benefit from pricing actions.

Motorhome RV was the offset, with revenues up 10.1% to $320.7 million. Patrick IndustriesPATK, a supplier to RV, marine, powersports and housing markets, provides another industry read-through because supplier demand often reflects production discipline across the same outdoor recreation ecosystem.

How WGO’s Ratings Frame the Debate

The bottom line is that WGO screens like a cheap cyclical stock, but the operating backdrop has not yet removed the value-trap risk. A low multiple can work in investors’ favor when earnings stabilize; it can also linger when guidance is falling.

The stock currently carries a Zacks Rank #4 (Sell). That rank points to a less favorable near-term earnings-revision profile, which matters for investors looking at the next one to three months rather than a longer-cycle recovery.

The Style Scores are more mixed. WGO has a Value Score of A, supporting the cheap-stock argument, along with a Growth Score of B and VGM Score of B. The weak Momentum Score of D and an unfavorable Zacks Rank make the signal profile difficult to overlook. Together, they suggest WGO’s low valuation may reflect persistent earnings pressure and weak market confidence rather than a clear contrarian setup.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).