WGO Stock Outlook Hinges on Motorhome RV Strength in 2026

Winnebago Industries, Inc.WGO is navigating a split 2026 backdrop. Motorhome improvement is helping, but the broader outdoor recreation market remains pressured.

The key question is whether product breadth and brand expansion can outweigh weak discretionary demand. For now, investors have to balance a visible bright spot against still-fragile towable RV and marine trends.

Winnebago's Segmental Split

Winnebago’s business is organized around three reportable segments: Towable RV, Motorhome RV and Marine. That mix matters because the company is not moving through the cycle evenly.

Towable RV represented 45.2% of fiscal 2025 revenues, while Motorhome RV accounted for 43.7%. Marine contributed 11.1%, making it smaller but still relevant to earnings quality, dealer demand and the company’s broader outdoor recreation identity.

Thor Industries, Inc. THO remains a direct RV peer because it also competes across towable and motorized recreational vehicles. Patrick Industries, Inc.PATK adds a supply-chain lens, since its component exposure to RV and marine markets makes it sensitive to the same production and dealer-order trends affecting Winnebago.

WGO Finds Support in New Products

Winnebago continues to lean on new products to defend share and broaden price-point coverage. In towables, the Access and Thrive platforms under the Winnebago brand and Grand Design’s Transcend Lite are aimed at expanding participation among buyers who remain price conscious.

The company is also refreshing the higher end of its portfolio. The ARKA off-grid adventure truck, updated Newmar offerings and Grand Design’s Worry-Free Roof technology support product differentiation in motorhomes and towables.

Marine is part of the same strategy. Barletta’s Sanza line creates a more accessible entry point into the brand while Barletta continues to build share in the U.S. aluminum pontoon segment.

Winnebago Gets a Lift From Motorhomes

The Motorhome RV segment is the clearest support point in Winnebago’s latest results. Segment revenues rose 10.1% year over year to $320.7 million in the fiscal third quarter of 2026.

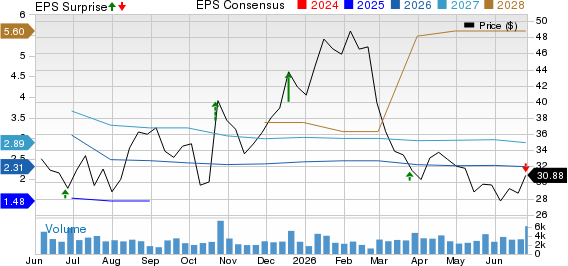

Winnebago Industries, Inc. Price, Consensus and EPS Surprise

Winnebago Industries, Inc. price-consensus-eps-surprise-chart | Winnebago Industries, Inc. Quote

The profit improvement was more important than the sales gain. Motorhome RV generated operating income of $9.6 million and a 3% operating margin, compared with an operating loss of $3.2 million and a negative 1.1% margin in the year-ago quarter.

Higher unit volume and selective price adjustments helped the segment, partly offset by higher input costs. Management also cited traction at Grand Design Motorized, execution at Newmar and broader share gains across key motorhome categories.

WGO Still Faces Demand Headwinds

The bullish case still runs into a difficult retail backdrop. Consumers remain interested in outdoor recreation, but affordability pressure, cumulative inflation, elevated interest rates and uncertainty around geopolitical events are delaying big-ticket purchases.

Dealer behavior is another drag. Management pointed to more deliberate ordering, with dealers focused on inventory quality, carrying costs and retail sell-through rather than adding wholesale volume.

These pressures are showing up outside motorhomes. Towable RV revenues fell 26.1% year over year in the fiscal third quarter of 2026, while Marine revenues declined 8.3%. Both segments also saw lower operating margins as volume deleverage, product mix and higher input costs weighed on performance.

What Winnebago’s Stock Signals Say Now

The bottom line is that Winnebago has one meaningful operating bright spot, but the stock still carries a weak short-term profile. Motorhome strength gives WGO a recovery argument, while towables, marine and consumer affordability keep that argument from looking clean.

WGO currently carries a Zacks Rank #4 (Sell). The Value Score of A supports the view that valuation screens well, and the Growth Score of B and VGM Score of B are not dismissive of the company’s broader financial profile.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

The Momentum Score of D keeps the signal mix cautious. Since Zacks Style Scores are designed to complement the Zacks Rank, the unfavorable rank makes it harder to treat WGO’s valuation as enough on its own. Investors may need clearer evidence that motorhome strength can spread across the portfolio before becoming more constructive.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).