Curaleaf Launches Buyback Program: Time to Get Bullish on the Stock?

Shares of Curaleaf Holdings CURLF have risen more than 25% in the past week since the company’s board of directors authorized an $83 million share repurchase program.

CURLF’s Buyback Program Aims to Enhance Shareholder Value

The share repurchase program allows the company to buy back as many as 34.4 million shares, or roughly 5% of its outstanding float, over the next 12 months. The program will be executed opportunistically in the open market, with repurchased shares set to be canceled, directly reducing the company’s share count.

The decision marks a notable shift in capital allocation strategy for the cannabis industry, where buybacks are uncommon due to limited access to capital, regulatory constraints, and a historical focus on expansion and liquidity preservation. The program signals management’s confidence in Curaleaf’s long-term prospects, while aiming to return value to its shareholders.

From a shareholder perspective, the implications are straightforward. Buybacks reduce the number of outstanding shares, which can support earnings per share (EPS) over time while helping stabilize stock performance in a volatile sector. In Curaleaf’s case, the program also sends a strong signaling effect — suggesting that management believes the stock is undervalued at the current levels.

The structure of the program further reinforces this disciplined approach. CURLF is not obligated to complete the full buyback, and purchases will depend on market conditions, liquidity and price levels. This flexibility allows Curaleaf to deploy capital efficiently while maintaining balance sheet strength — a critical factor in an industry where financial resilience remains a key differentiator.

However, investors should avoid drawing conclusions based solely on this single development. A deeper look at the company’s broader fundamentals is essential to determine how to position the stock following this announcement.

International Momentum May Not Offset CURLF’s Soft US Market

While Curaleaf Holdings continues to deliver strong growth in its international segment, the company’s overall performance remains weighed down by persistent weakness in its core U.S. operations.

For full-year 2025, Curaleaf generated approximately $172 million in international revenues, representing a robust 63% year-over-year increase, driven primarily by expansion across European medical cannabis markets, particularly the U.K. and Germany. This growth has been supported by rising patient enrollment, broader physician adoption, and continued strength in Curaleaf’s branded product portfolio. However, despite this strong trajectory, the international segment remains relatively small, accounting for only about 14% of the total 2025 revenues of $1.27 billion.

In contrast, Curaleaf’s U.S. business — which still represents the bulk of revenues — continues to face significant headwinds. The company is navigating a challenging pricing environment across key markets, marking the third consecutive year of industry-wide price compression amid ongoing regulatory uncertainty.

As a result, international growth, while impressive, has not been sufficient to offset domestic pressure meaningfully. The company’s consolidated performance remains heavily tied to U.S. market dynamics, limiting the overall impact of its faster-growing international operations.

Looking ahead, management remains optimistic about international expansion, citing continued demand growth in core European markets and long-term opportunities in regions such as France, Spain and Turkey. However, these newer markets are unlikely to contribute meaningfully in the near term, reinforcing the view that international momentum will remain supportive — but not enough to materially change Curaleaf’s near-term financial trajectory.

Stiff Competition From Peers

Curaleaf operates in an increasingly saturated U.S. cannabis market, where price compression and oversupply are weighing on nearly all players. The company faces stiff competition from peers like Green Thumb GTBIF and Tilray Brands TLRY.

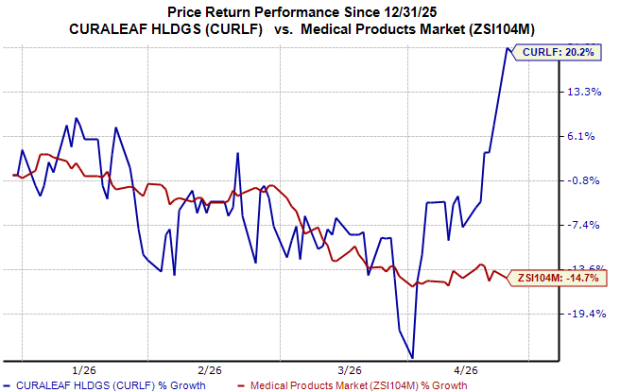

CURLF Stock Performance and Estimates

Year to date, shares of Curaleaf Holdings have risen 20% against the industry’s 15% decline.

Image Source: Zacks Investment Research

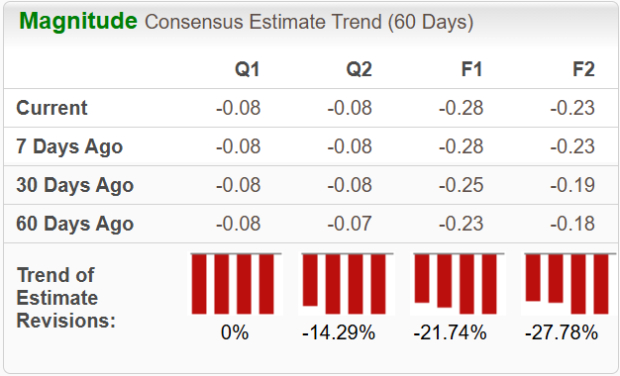

Loss estimates for 2026 and 2027 have widened over the past 30 days.

Image Source: Zacks Investment Research

How to Play CURLF Stock?

While Curaleaf Holdings benefits from a stable revenue base and positive free cash flow generation, its heavy exposure to the U.S. market remains a key overhang. Persistent pricing pressure, combined with intense competition in an increasingly saturated cannabis landscape, continues to pressure margins and delay a return to consistent profitability. Although recent developments around potential marijuana rescheduling have reignited optimism in the cannabis sector, the company’s underlying fundamentals have yet to show meaningful improvement.

Recent downward revisions in EPS estimates suggest a pessimistic analyst outlook for the stock in the near term. Curaleaf carries a Zacks Rank #4 (Sell), suggesting limited upside and elevated risk for investors at present.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).