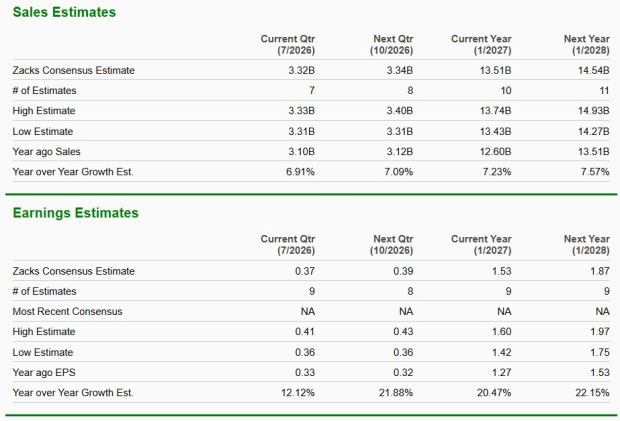

Is CHWY Stock a Buy After Its Selloff and Lower Revenue View

Chewy, Inc.CHWY has become harder to frame after a sharp selloff and lower fiscal 2026 revenue outlook.

The question is whether the decline has created a better entry point or whether softer consumer behavior still argues for patience. Investors need to weigh valuation against recurring revenue strength, margin progress and execution risk.

Why CHWY Looks Cheaper on Sales Multiples

CHWY, which carries a Zacks Rank #4 (Sell), trades at 0.56X forward 12-month sales. That is well below the Zacks sub-industry at 1.99X, the Zacks sector at 1.50X and the S&P 500 at 5.17X. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The stock is also near the low end of its five-year sales multiple range. CHWY has traded as high as 4.01X, as low as 0.55X and at a median of 1.18X. That helps explain why some investors may see less downside from valuation compression after the stock’s 42.9% year-to-date decline and 54.6% slide over the past year.

Why Chewy Still Supports a Bullish Case

Chewy’s bull case still starts with Autoship, which gives the business a recurring revenue base that many retailers lack. In the first quarter of fiscal 2026, Autoship customer sales rose 10.5% year over year to $2.83 billion and represented 84.4% of net sales.

Customer metrics remain supportive. Active customers increased 3.6% year over year to 21.5 million, while net sales per active customer reached $597. Pet health, SmartPak and Modern Animal add another layer by expanding Chewy beyond core online retail and into higher-engagement services.

Profitability also keeps the debate from turning one-sided. First-quarter adjusted EBITDA rose 31.3% to $253.1 million, and adjusted EBITDA margin expanded 130 basis points to 7.5%. Fiscal 2026 adjusted EBITDA margin guidance of 6.6-6.8% still implies about 100 basis points of expansion at the midpoint.

Image Source: Zacks Investment Research

Why CHWY Still Warrants Investor Caution

The risk is that valuation may not be enough if sales expectations keep moving lower. Chewy reduced its fiscal 2026 net sales outlook to $13.40-$13.55 billion from $13.6-$13.75 billion, even with expected acquisition contributions.

Management cited pressure on premiumization and product attachment rates among existing customers. That matters because net sales per active customer is a key growth driver, and a cautious consumer could keep discretionary categories under pressure.

Near-term margin cadence is less clean. Second-quarter gross margin is expected to contract modestly year over year due to difficult comparisons. Acquisition and integration costs, a modest margin drag from Modern Animal and $10-$15 million of expected fiscal 2026 net interest expense from the Term Loan B add to the caution.

What Could Change the Chewy Stock Debate

The most important signal would be stabilization in consumer spending. If premiumization and attachment rates improve, pressure on net sales per active customer could ease.

Customer additions are another checkpoint. Chewy, which competes with Petco Health and Wellness CompanyWOOF and Central Garden & Pet CompanyCENT, still expects net additions near the lower end of the prior 150,000-250,000 quarterly range, so stronger customer growth would help support confidence in share gains.

Execution in health is equally important. SmartPak is expected to contribute $80 million to fiscal 2026 net sales, while Modern Animal is expected to add $70 million. Investors should also watch whether artificial intelligence-driven efficiencies, expected to contribute low tens of millions of dollars in fiscal 2026, support cost savings.

How the Zacks View Frames CHWY Today

The bottom line is that CHWY looks inexpensive on sales, but not risk-free. A 0.56X forward sales multiple is hard to ignore, yet the lower revenue view shows that cheaper valuation has not offset weaker demand signals.

The Zacks view is Neutral, indicating a balanced stance rather than a decisive buy signal after the selloff. That fits a stock with recurring revenue, improving margins and healthcare expansion, but also softer consumer trends and added execution costs.

For investors who lean on the Zacks Rank and Zacks Style Scores, the clearest signal here is the Neutral view. Style Scores complement the Zacks Rank across value, growth and momentum characteristics, but valuation alone has not yet overridden the company’s near-term demand concerns.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).