Can Margin Strength Offset Demand Challenges at Home Depot?

The Home Depot Inc.’s HD ability to sustain margin strength is becoming increasingly important as demand across the home improvement sector remains subdued. In the first quarter of fiscal 2026, the company reported sales growth of 4.8% to $41.8 billion, while comparable sales inched up 0.6%, reflecting a demand environment that management described as largely unchanged from fiscal 2025. Housing affordability pressures, elevated mortgage rates, and muted large-scale remodeling activity continue to weigh on customer spending.

Despite these headwinds, Home Depot is demonstrating resilience through operational execution and strategic investments. The company continues to gain market share, supported by strength in professional customers, digital sales growth exceeding 10% and expanding capabilities through acquisitions such as SRS, GMS and Mingledorff’s. Management highlighted that Pro sales outperformed DIY demand, with complex purchase occasions showing strongest growth, underscoring the effectiveness of its “winning the Pro” strategy.

From a margin perspective, the fiscal first-quarter gross margin declined 75 basis points (bps) to 33% due to the GMS acquisition and pricing investments at SRS. However, management emphasized that the core Home Depot business maintained a stable margin profile, while reaffirming its full-year gross margin guidance of 33.1% and the adjusted operating margin outlook of 12.8-13%.

The key question is whether margin stability can compensate for sluggish demand. While disciplined cost management, operational efficiencies and a richer Pro mix can help protect profitability, sustained earnings growth will ultimately require stronger project demand. For now, Home Depot’s margin resilience, market-share gains and strategic expansion provide a meaningful buffer against demand challenges, allowing the company to navigate a prolonged housing downturn while positioning itself for growth.

How Are LOW & WSM Faring in Terms of Profit Margins?

While Home Depot has long been known for its strong profitability, investors are also closely watching how peers Lowe’s Companies Inc.LOW and Williams-Sonoma Inc.WSM are performing on the margin front amid a challenging demand environment.

Lowe’s is facing weak DIY demand, elevated rates and low housing turnover, but margin discipline is helping cushion the pressure. In first-quarter fiscal 2026, comps rose 0.6%, while the gross margin fell 70 bps to 32.7% due mainly to acquisition dilution. SG&A leveraged 17 bps, supported by cost controls and productivity initiatives. Management reaffirmed its 11.6-11.8% adjusted operating margin outlook, signaling confidence despite demand challenges.

Williams-Sonoma is demonstrating that strong margins can help offset broader demand uncertainties. In first-quarter fiscal 2026, the company posted a 4.8% comps increase and delivered an operating margin of 16.2%, exceeding expectations despite absorbing higher tariffs and fuel costs. Supply-chain efficiencies, disciplined cost management and strong full-price selling helped mitigate margin pressures. While management remains cautious about the macro environment, its profitability and execution provide a meaningful cushion against demand volatility.

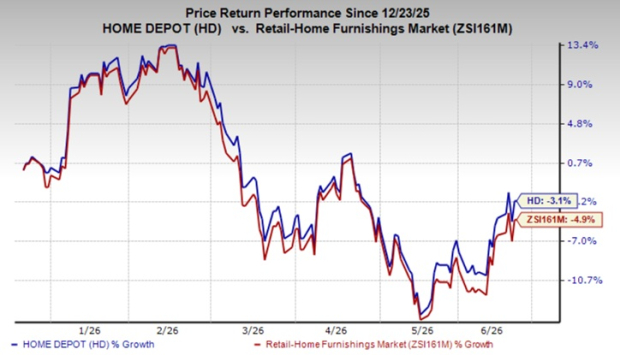

HD’s Price Performance, Valuation & Estimates

Shares of Home Depot have lost 3.1% in the past six months versus the industry’s decline of 4.9%.

Image Source: Zacks Investment Research

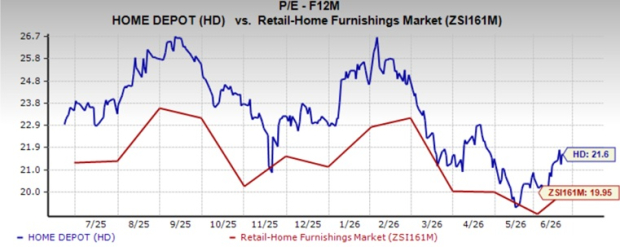

From a valuation standpoint, HD trades at a forward price-to-earnings ratio of 21.6X compared with the industry’s average of 19.95X.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for HD’s fiscal 2026 and fiscal 2027 EPS implies year-over-year growth of 4.2% and 2.2%, respectively. The company’s EPS estimates for fiscal 2026 and 2027 have moved down 0.3% and 0.9%, respectively, in the past 60 days.

Image Source: Zacks Investment Research

Home Depot currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).