Here's Why You Should Retain BDX Stock in Your Portfolio Now

Becton, Dickinson and Company BDX is benefiting from its focused transformation into a pure-play MedTech company, supported by strong execution of its BD 2025 strategy. The company’s continued emphasis on innovation, strategic partnerships and solid second-quarter fiscal 2026 results are driving optimism. However, persistent reimbursement uncertainties, macroeconomic headwinds and stiff competition remain key concerns.

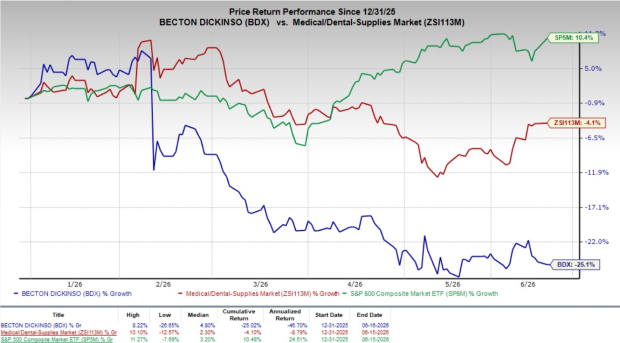

This Zacks Rank #3 (Hold) stock has lost 25.1% in the year-to-date period compared with the industry’s 4.1% decline. The S&P 500 Composite has returned 10.4% during the same time frame.

The renowned medical technology player, with a market capitalization of $40.30 billion, remains focused on delivering durable growth and margin expansion. It projects 8.96% growth for the next fiscal year and expects to maintain a strong performance in the future. BDX’s earnings surpassed the Zacks Consensus Estimate in the trailing four quarters, the average being 4.13%.

Image Source: Zacks Investment Research

Reasons Favoring BDX’s Growth

Strategic Execution Under the New BD Framework: Following the separation of its Biosciences and Diagnostic Solutions business and combination with Waters, the company is executing its New BD strategy as a focused MedTech company. The company’s priorities — Compete, Innovate and Deliver — are aimed at strengthening commercial execution, accelerating innovation and improving operational efficiency. Management remains focused on driving sustainable growth, margin expansion and long-term shareholder value.

The strategy is already yielding results. In second-quarter fiscal 2026, more than 90% of Becton, Dickinson’s portfolio delivered mid-single-digit growth, while key growth platforms such as biologic drug delivery, Advanced Patient Monitoring, PureWick and advanced tissue regeneration posted double-digit gains. The company has also achieved $150 million of its $200-million cost-out program, supporting profitability and cash flow generation.

Continued Focus on Innovation and R&D: Becton, Dickinson continues to invest heavily in R&D, clinical development and regulatory capabilities to strengthen its product pipeline and competitive position. The company is expanding the use of its BD Excellence operating system within R&D, helping reduce development timelines and accelerate product launches.

Recent initiatives highlight this commitment. BDX invested $110 million to expand prefillable syringe production for biologics and GLP-1 therapies, completed a sustainability-focused collaboration with Envetec and expanded the European indication of Phasix Mesh. In addition, launches such as the HemoSphere Stream Module, EnCor EnCompass Biopsy System and Revello Vascular Covered Stent are expanding addressable markets and supporting long-term growth.

Strategic Partnerships & Product Launches: Becton, Dickinson has strengthened its market position through collaborations, acquisitions and product introductions. Partnerships with Wellstar Health System and Sinteco are enhancing medication management and pharmacy automation capabilities, while the successful completion of the Waters transaction reaches a milestone in the BD 2025 strategy.

The company has also expanded its innovation portfolio through launches such as the Elyra Thulium Fiber Laser System, BD CentroVena One Insertion System and AI-enabled BD Research Cloud 7.0. These initiatives are expected to enhance customer adoption, strengthen competitive positioning and support future revenue growth.

Factors That May Offset BDX’s Gains

Macroeconomic Headwinds: Becton, Dickinson faces risks from inflation, tariffs, supply-chain disruptions and geopolitical uncertainties. Persistent cost pressures and changes in global trade policies could increase operating expenses, disrupt production and weigh on healthcare spending.

Reimbursement Challenges: Demand for the company’s products depends partly on reimbursement policies and insurance coverage. Increasing pricing scrutiny, value-based payment reforms and healthcare budget constraints may limit product adoption, pressure pricing and reduce procedure volumes.

Intense Competition & Foreign Exchange Exposure: Becton, Dickinson operates in a highly competitive medical technology market characterized by rapid innovation, industry consolidation and pricing pressure from low-cost manufacturers. Significant international operations expose the company to foreign currency fluctuations, which can adversely impact revenues, profitability and cash flows despite hedging efforts.

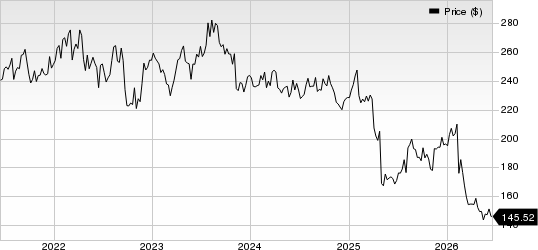

Becton, Dickinson and Company Price

Becton, Dickinson and Company price | Becton, Dickinson and Company Quote

Estimate Trend

Becton, Dickinson is witnessing a stable estimate revision trend for fiscal 2026. In the past 30 days, the Zacks Consensus Estimate for its earnings has been unchanged at $12.61 per share.

The Zacks Consensus Estimate for the company’s third-quarter fiscal 2026 revenues is pegged at $4.89 billion, indicating an 11.2% decline from the year-ago quarter’s reported number.

Key Picks

Some better-ranked stocks from the same medical industry are Align Technology ALGN, West Pharmaceutical Services WST and Cardinal Health CAH.

Align Technology, sporting a Zacks Rank #1 (Strong Buy) at present, has an estimated long-term growth rate of 10.3%. ALGN’s earnings surpassed estimates in three of the trailing four quarters and missed once, the average surprise being 7.80%. You can see the complete list of today’s Zacks #1 Rank stocks here.

ALGN shares have gained 14.1% against the industry’s 4.2% decline in the year-to-date period.

West Pharmaceutical, currently flaunting a Zacks Rank of 1, has an estimated long-term growth rate of 13.9%. WST’s earnings surpassed estimates in the trailing four quarters, the average surprise being 19.37%.

West Pharmaceutical’s shares have gained 20.4% against the industry’s 4.2% decline year to date.

Cardinal Health, currently carrying a Zacks Rank #2 (Buy), has an estimated long-term growth rate of 17%. CAH’s earnings surpassed estimates in the trailing four quarters, the average surprise being 10.27%.

CAH shares have gained 10.1% against the industry’s 4.2% decline so far this year.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).