Post Holdings' Foodservice Business: Is it the Key Growth Engine?

Post Holdings, Inc.’s POST Foodservice segment continues to be a significant contributor to the company’s portfolio, with management identifying a target adjusted EBITDA run rate of approximately $125 million per quarter. While the company does not provide specific guidance for individual segments, they expect to return to this run rate as market supply and demand remain in balance.

Recent performance benefited from a combination of factors, including the lapping of prior-year HPAI-related supply constraints and periods when costs exceeded pricing, as the business moved toward more balanced market conditions.

The company’s value-added products appear to benefit from strong customer stickiness, particularly among larger operators. Once customers adopt these offerings, they are able to reduce labor requirements while benefiting from greater consistency and food safety, making switching less likely.

Management noted that smaller independent operators may present some risk due to their greater operational flexibility and ability to revert to alternative approaches. However, the company believes that the majority of its customer portfolio exhibits durable retention characteristics.

Furthermore, the Foodservice business provides strategic infrastructure that supports other segments. Specifically, the Michael Foods assets are leveraged to support growth of the Bob Evans refrigerated business. This synergy allows Post Holdings to leverage existing manufacturing capabilities while evaluating opportunities to expand into additional categories. Overall, Post Holdings’ Foodservice segment remains an important contributor to company performance, supported by value-added products, durable customer relationships and operational connections across the broader portfolio.

The Zacks Rundown for POST

The company’s shares have lost 6.7% in the year-to-date period compared with the industry’s 2.9% decline.

Image Source: Zacks Investment Research

From a valuation standpoint, POST trades at a forward price-to-earnings ratio of 10.97, lower than the industry’s average of 14.14. POST currently carries a Zacks Rank #3 (Hold).

Image Source: Zacks Investment Research

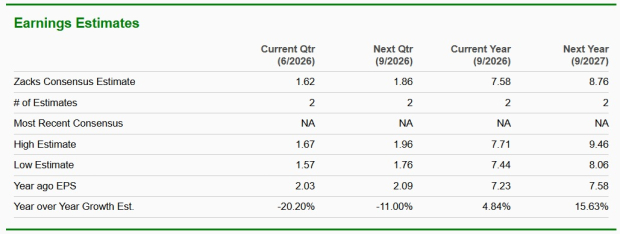

The Zacks Consensus Estimate for POST’s current and next fiscal year earnings implies a year-over-year increase of 4.8% and 15.6%, respectively.

Image Source: Zacks Investment Research

Stocks to Consider

Some better-ranked stocks have been discussed below:

The Chef’s Warehouse, Inc.CHEF distributes specialty food and center-of-the-plate products in the United States, the Middle East, and Canada. CHEF currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for CHEF’s current fiscal-year sales and earnings indicates growth of 8.3 and 24.7%, respectively, from the year-ago reported figures. CHEF delivered a trailing four-quarter earnings surprise of 28.9%, on average.

Armanino Foods of Distinction, Inc.AMNF produces and markets frozen food products in the United States. AMNF currently carries a Zacks Rank #2 (Buy).

The Zacks Consensus Estimate for Armanino Foods' current fiscal-year sales and earnings indicates growth of 7% and 1.7%, respectively, from the year-ago actuals. AMNF delivered a trailing four-quarter earnings surprise of 23.1%, on average.

Mama’s Creations, Inc.MAMA, together with its subsidiaries, manufactures and markets fresh deli-prepared foods in the United States. MAMA currently carries a Zacks Rank #2.

The Zacks Consensus Estimate for MAMA's current fiscal-year sales & earnings implies growth of 30% and 73.3%, respectively, from the year-ago actuals. MAMA delivered a trailing four-quarter negative earnings surprise of 129.2%, on average.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).